🧵While we in Fintech are Hoping for Challenger/Neo Banking Licences from RBI. Let's understand more about Small Finance Bank and from their success, try to see if a balance between Profitability (for business) and Financial Inclusion (for RBI) can be made for future usecase?👇

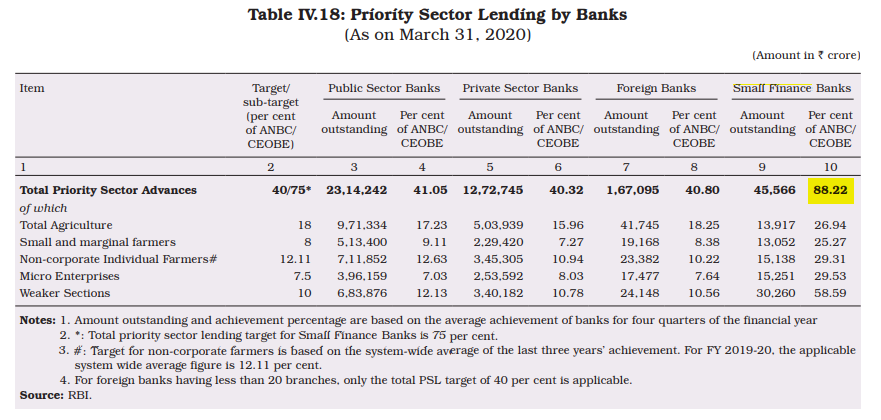

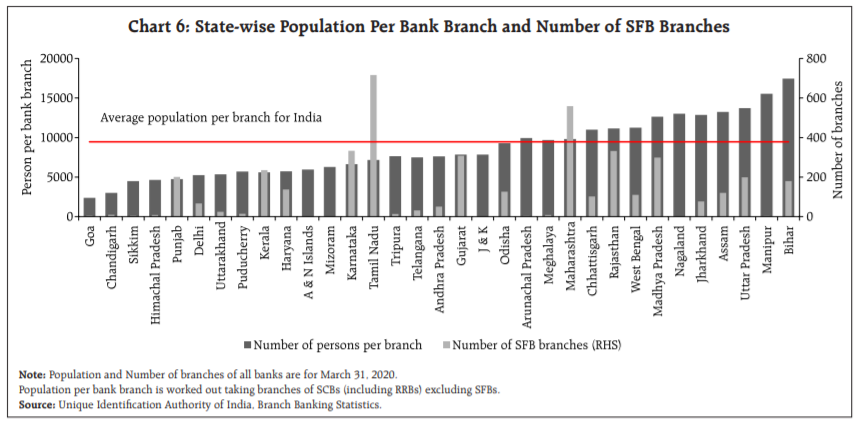

1. Priority Sector Lending (75% of their total lending) and 2. Branches for Unbanked (SFB were required to have 25% of their branches in rural unbanked centres (population shall be less than 10,000)

More from Business

You May Also Like

These 10 threads will teach you more than reading 100 books

Five billionaires share their top lessons on startups, life and entrepreneurship (1/10)

10 competitive advantages that will trump talent (2/10)

Some harsh truths you probably don’t want to hear (3/10)

10 significant lies you’re told about the world (4/10)

Five billionaires share their top lessons on startups, life and entrepreneurship (1/10)

I interviewed 5 billionaires this week

— GREG ISENBERG (@gregisenberg) January 23, 2021

I asked them to share their lessons learned on startups, life and entrepreneurship:

Here's what they told me:

10 competitive advantages that will trump talent (2/10)

To outperform, you need serious competitive advantages.

— Sahil Bloom (@SahilBloom) March 20, 2021

But contrary to what you have been told, most of them don't require talent.

10 competitive advantages that you can start developing today:

Some harsh truths you probably don’t want to hear (3/10)

I\u2019ve gotten a lot of bad advice in my career and I see even more of it here on Twitter.

— Nick Huber (@sweatystartup) January 3, 2021

Time for a stiff drink and some truth you probably dont want to hear.

\U0001f447\U0001f447

10 significant lies you’re told about the world (4/10)

THREAD: 10 significant lies you're told about the world.

— Julian Shapiro (@Julian) January 9, 2021

On startups, writing, and your career: