$TSLAQ Instead of having an accrual palooza, I will dribble these out as I have time and available information. The first account to be reviewed: Automotive Leasing Revenues. The remainder of the planet calls this Sales-Type Leasing (ASC 842.) (1/n)

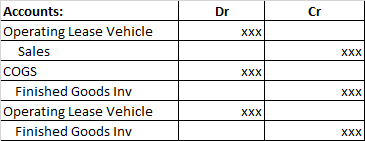

GAAP allows revenue recognition if a manufacture or dealer leases the preponderance of useful life and economic value of inventory. Computer manufactures are significant users of this accounting treatment. The journal entries for this type of leasing are: (2/n)

The sales are the present value of the payments plus down payment. COGS is the cost of the equipment less the present value of the residual payment. (3/n)

The final receivable entry is the residual value added to the lease payment receivable to remove inventory from the financial statements. $TSLA classifies the lease receivable as an Operating Lease Vehicles, net on the balance sheet and they are subject to depreciation. (4/n)

The assumptions in the calculation that can be subject to manipulation: the implicit interest rate of the lease and the residual payments. Lower rates increase capitalization of the lease which gives higher revenues. Larger residual decreases cost of goods sold. (5/n)