Open Question to fellow investors tracking Music Industry.

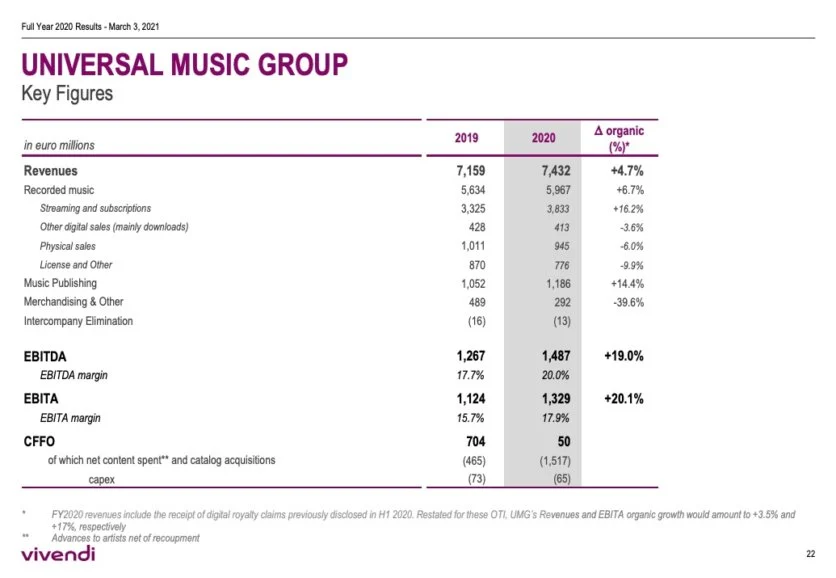

A business like Universal which controls more than 1/3rd of all published music globally is selling for less than 6x FY20 Sales.

Why are Indian businesses like Saregama / Tips selling for 11x, 20x their sales?

FY 20 Revenues ~ 8.87 B USD or 7.4B EUR

Catalogue of Music includes every international artist you can possibly name

Either Universal is grossly undervalued or Saregama/Tips are grossly overvalued.

Homework for all the interested participants here:

— Intrinsic Compounding (@soicfinance) June 27, 2021

Q1.Why 20% and not 50%+ Margins for UMG

Q2. Differences in dynamics between Western&Indian cos?

Q3. Trends in West vs Trends in India in the industry.

Research and find the answers. My job is done \U0001f601\U0001f64f

If you see the ebitda of universal music its low 20% compared to our saregama 30% or tips 50%. So when you compare earnings saregama is 40x and tips is 30x and universal music is 30x. Also these type of companies are less( low or no capex with excellent and growinh cashflows)

— Srikanth V (@mynameisnani75) June 27, 2021

The rights are different here in India.

— Saket Reddy (@saketreddy) June 27, 2021

Indian labels own both publishing and master rights unlike the global peers.

Hence the 80% EBITDA Margins vs 20% EBITDA Margins for UMG.

Comparing them isn't useful IMO but should be only referred to study the Industry structure.

1. You own both the recording and publishing rights in India

— Saket Mehrotra \U0001f60e\u2615\U0001f4b0 (@mehrotra_saket) June 27, 2021

2. Streaming business in India is 85% of the industry compared to 52% globally

3. You should look at FY21 number for Tips as that is pure-play music streaming

4. Headroom in India builds optional value for paid converts https://t.co/mOBj83uZgH

All throughout the world, largecaps sell at lower valuations than smallcaps. Larger room for growth. + India growth narrative. + More rights with labels in India. + The whole bollywood industry means that imo moat is wider in india for indian labels than at global stage for umg

— Sahil Sharma (@sahil_vi) June 27, 2021

I think valuations based on sales is suitable only when the current profitability does not reflect the true profitability of the business. In the end valuations are based on profits

— Ankush Agrawal (@Ankush__Agrawal) June 28, 2021

UMG and Tips have very different margins and thus comparison based on sales is not a great way 1/2

Why do you think Bill Ackman is pouring in 28000 crore in Universal? He clearly believes that even at 25x EV/EBITDA, it is CHEAP.

— Neil Bahal (@NeilBahal) June 27, 2021

Universal has 20% ebitda margin. Tips has 60% net profit margin :) :) pic.twitter.com/6y8mEoLAU6

More from Tar ⚡

Case Study: Bharat Electronics Ltd

OPM: 23%

Free Float: <5%

QoQ continuous increase in ownership by institutions

ROE: ~20%

ROCE: ~28%

EV by EBITDA: 15

Leading developer of Indigenous Military Drones

Exports are prime focus for the company

D: Invested, not a recommendation

OPM: 23%

Free Float: <5%

QoQ continuous increase in ownership by institutions

ROE: ~20%

ROCE: ~28%

EV by EBITDA: 15

Leading developer of Indigenous Military Drones

Exports are prime focus for the company

D: Invested, not a recommendation

Lots of under owned stocks with robust financials within Defense Sector \U0001fa96\U0001f396\ufe0f

— Tar \u26a1 (@itsTarH) April 12, 2022

You don't even have to try looking very hard to find something interesting

More from Music

You May Also Like

A list of cool websites you might now know about

A thread 🧵

1) Learn Anything - Search tools for knowledge discovery that helps you understand any topic through the most efficient

2) Grad Speeches - Discover the best commencement speeches.

This website is made by me

3) What does the Internet Think - Find out what the internet thinks about anything

4) https://t.co/vuhT6jVItx - Send notes that will self-destruct after being read.

A thread 🧵

1) Learn Anything - Search tools for knowledge discovery that helps you understand any topic through the most efficient

2) Grad Speeches - Discover the best commencement speeches.

This website is made by me

3) What does the Internet Think - Find out what the internet thinks about anything

4) https://t.co/vuhT6jVItx - Send notes that will self-destruct after being read.