2/ Chipotle is the leading fast casual restaurant chain across the US, with almost 3,000 owned & operated locations

They benefit from strong unit economics and a trusted brand

We'll discuss consensus estimates, competitive landscape, and expected value

https://t.co/iVFnS9dyRg

3/ We must first identify the price-implied expectations based on key value drivers

After finding the consensus estimates, investors can seek opportunities in the expectations - looking for a divergence from the market's assumptions

Let's start with Chipotle's sales growth

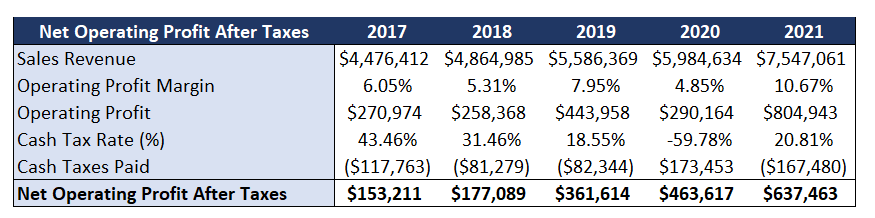

4/ Chipotle has grown revenues from $3.9B to $7.55B over the past 5 years, at a 5 year CAGR of 14.1%

Analysts estimate a 13.7% consensus growth rate based on 5-7% same store sales growth, 8% additional store openings per year, and steady digital sales contribution

5/ Next is operating profit margin, which measures profitability from core operations

Chipotle has slowly been growing its margin, now at 10.67%

Analysts expect high margins of 15.75%, with incremental profits from digital orders and unit-level margin growth contributing

6/ The cash tax rate measures what the company paid in taxes, after any benefits like SBC

Cash taxes trailed income taxes slightly over the cumulative 5 year period, with small tax benefits

Future cash taxes are estimated at 25% based on historical rates and company guidance

7/ With these 3 initial metrics, we can solve for net operating profits after taxes (NOPAT), or the profits a business made from core operations, after taxes

Historical NOPAT has grown meaningfully, almost 4x the 2017 figure

On to investments...

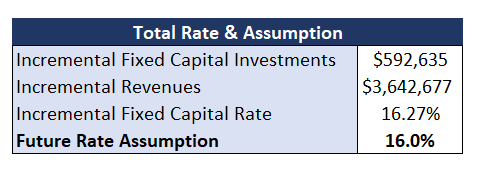

8/ Incremental fixed capital is the additional investment a business makes into PPE and long term assets each year

For Chipotle that's store openings, improvements to existing stores, and technology

To earn an extra dollar in sales, Chipotle invested 16 cents (16% rate) in PPE

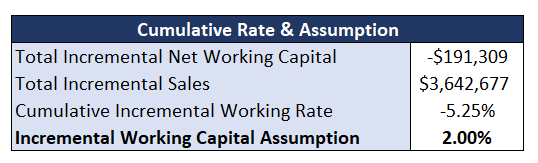

9/ Incremental working capital is the additional investment into current assets funding operations, such as accounts payables or wages

Chipotle benefits from negative working capital, where suppliers finance their operations at no cost (float)

Gift cards are $130mm of float too

10/ To dig deeper, Chipotle has a negative cash conversion cycle, which means they are receiving payment from customers BEFORE paying out suppliers

Pretty great getting an interest free loan

Suppliers and customers finance Chipotle's operational growth

11/ To bring it all together, total net working capital over the 5 year period was -$191mm, and the incremental sales added were $3.6B

This resulted in a negative incremental working capital rate at -5.25%.

I conservatively chose 2% for the future estimate

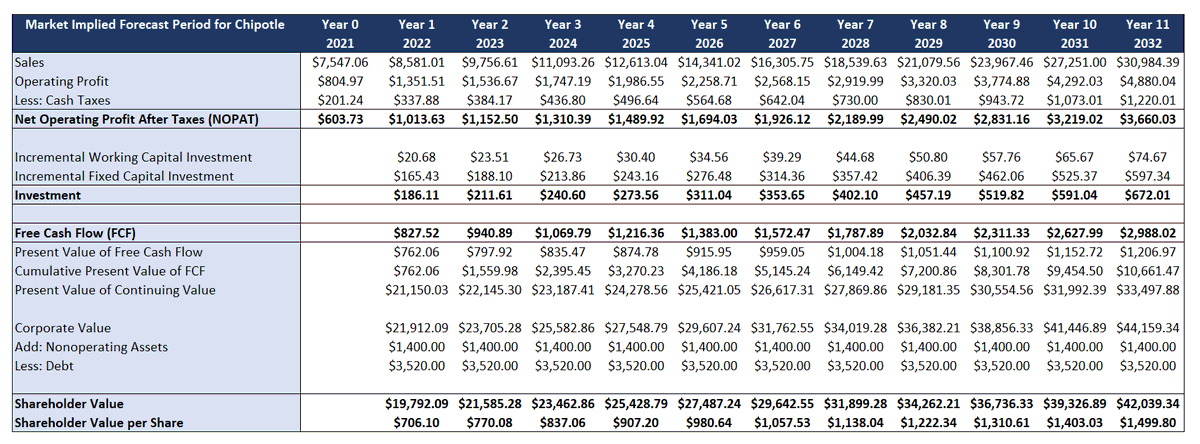

12/ We now can calculate free cash flow by subtracting our NOPAT - investments

Chipotle's free cash flow has grown at a 22% CAGR, from $152mm in 2017 to $415mm in 2021

Now we need our cost of capital...

13/

@AswathDamodaran provided incredible guidance for understanding cost of capital on

@10kdiver's Money Concepts session

He shared cost of capital's role in discounting, as a company investment hurdle, and how it relates to portfolio risk

A must listen:

https://t.co/nyABNKeqa4

14/ Damodaran found that 80% of companies had a cost of capital between 5.23% and 10%, with 50% of firms within 1.5% of an 8% WACC (weighted average cost of capital)

He recommends spending more time on value drivers rather than perfecting the WACC

My WACC for Chipotle is 8.59%

15/ With all our consensus estimates, we can now find the market implied forecast period - which tells us how many years it takes to reach today's share price

Chipotle is expected to reach their $1475 current share price by year 11, with 3-4x in revenues & FCF

16/ Before we run sensitivity tests, we should better understand the competitive landscape

An industry map shows the key constituents, such as landlords, staff, ingredient suppliers, tech providers, and competitors

17/ We can also look at their position in the overall market, where Chipotle leads fast casual

In a market segment growing 12% annually, Chipotle is in a good position to continue their success

18/

@zbfuss discussed how Chipotle counter-positioned competitors by targeting an underserved market, using a price x service quadrant framework

Chipotle has dominated the quick service, higher price & quality segment for a decade now

https://t.co/2rC22YwqL6

19/ Chipotle has strong unit economics

It costs Chipotle $1mm to build a new location

That store makes $2.6mm in annual revenue, with a 22.5% margin

This results in $585k in annual operating income, which after taxes and CapEx, is closer to $365k in free cash flow per store

20/ Competitively, Chipotle benefits from scale, brand, tech integration, and culture

Scale drives down costs and means negative cash conversion cycles

Brand lowers CAC

Digital leads to repeat & larger orders

Culture ensures happy employees, happy customers

21/ With a better understanding of competitive dynamics, we can select Chipotle's turbo trigger

The turbo trigger is the value driver that has the largest variance in expectations and share prices

For Chipotle, that is the operating profit margin

22/ The consensus estimate for operating profit margin already prices in a 500 bps increase

The low scenario is 10.5%, which is level to today

The high scenario is 17.5%, which factors in better digital margins and incredible unit margins

23/ With these in mind, we can attach probabilities based on our own beliefs and find the expected value

I selected the consensus estimates with a slight edge towards bearish

The expected value was $1400, below today's share price

24/ We’re still able to walk away with a much better understanding of the business after the expectations process

Mauboussin covers much more in the book, like competitive strategy, psychological biases, M&A, real options, and buybacks! 🤯

His big ideas -https://t.co/OG1qo84ABo

25/ Dive deeper into Chipotle and his expectations investing process here -

https://t.co/iVFnS9dyRg I go into detail on the financial estimates and how competitive powers have differentiated Chipotle

Hope you enjoy it!