PG Electroplast Limited, a contract manufacturer of various kinds of electrical goods and appliances, recently announced an 80 crore fund-raise through preferential allotment of equity shares and compulsorily convertible debentures (CCD) to Baring PE and family funds. (2/n)

Such transactions are a great way to understand Private Equity deals in a public setting. Because of disclosure norms for listed companies, everything related to a fund infusion in a listed company is made available to the public. (3/n)

From a retail investor’s perspective, it is easy to focus only on WHO is investing. In this thread, I will try to look at such a transaction from the perspective of all stakeholders – the company, the PE investors, and the public shareholders. (4/n)

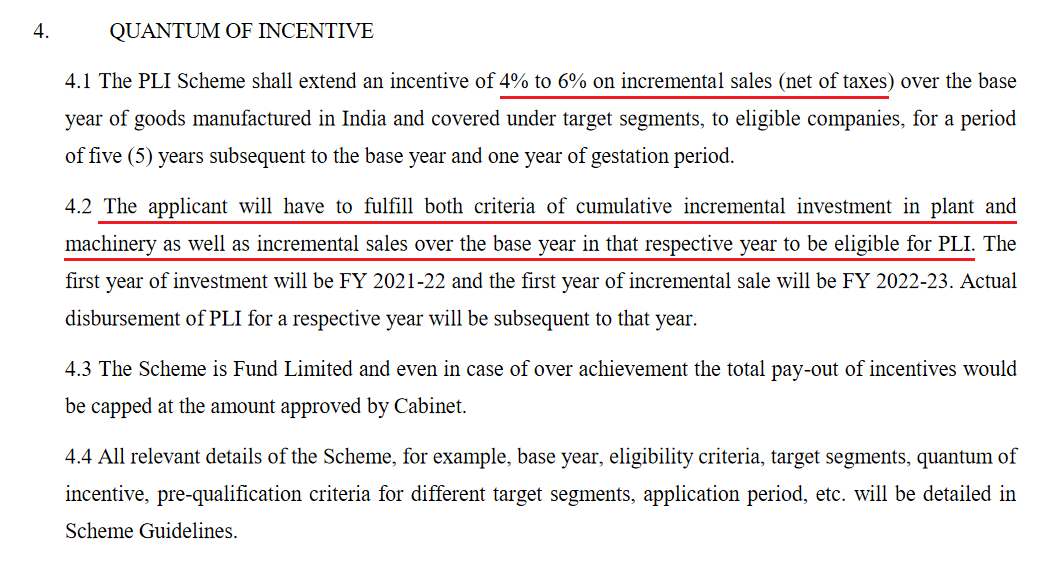

PG Electroplast sees an opportunity in the Productivity-Linked Incentives (PLI) by GoI. Under this scheme, companies making incremental investments into manufacturing facilities receive up to 6% of the incremental sales generated from such investment as an “incentive”. (5/n)

The PLI scheme is direct transfer to companies as a reward for expanding manufacturing operations in India. You do not get the incentive just for buying machinery and equipment though, the incentive is linked to the incremental sales generated from the investment. (6/n)

So, you must tell the government exactly how much you will be investing over 5 years, execute the capex plan and start selling the manufactured goods. Once you have achieved sales, you claim the eligible incentive from the government. This is a back-ended subsidy. (7/n)

PG Electroplast likely lies in the highlighted category of 'normal investment' in the White Goods PLI scheme. If the company invests as per the schedule in the scheme and also achieve the incremental sales targets, it can claim INR 180-200 crore as incentives over 5 years. (8/n)

It is interesting to note that PGE will need to invest INR 250-300 crore and achieve cumulative incremental sales of INR 3750-4125 crore over 5 years to achieve the full incentives. Every 1 Rupee invested will need to generate 5 Rupees of sales. (9/n)

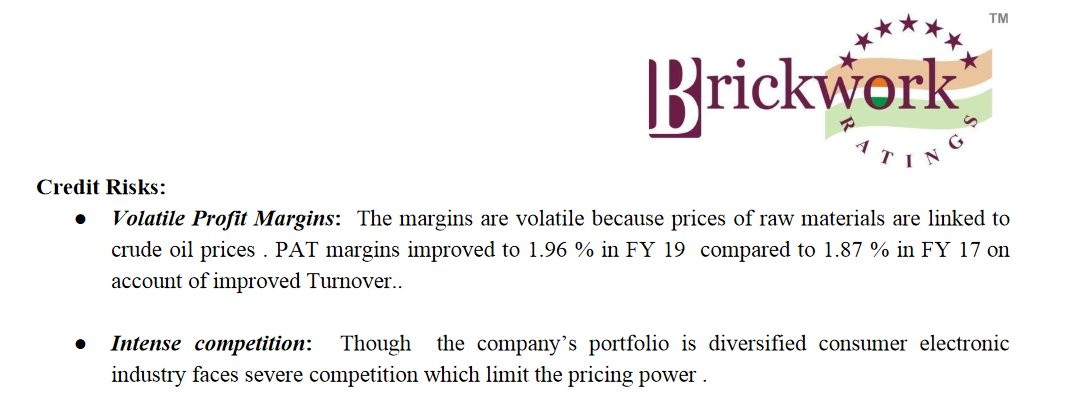

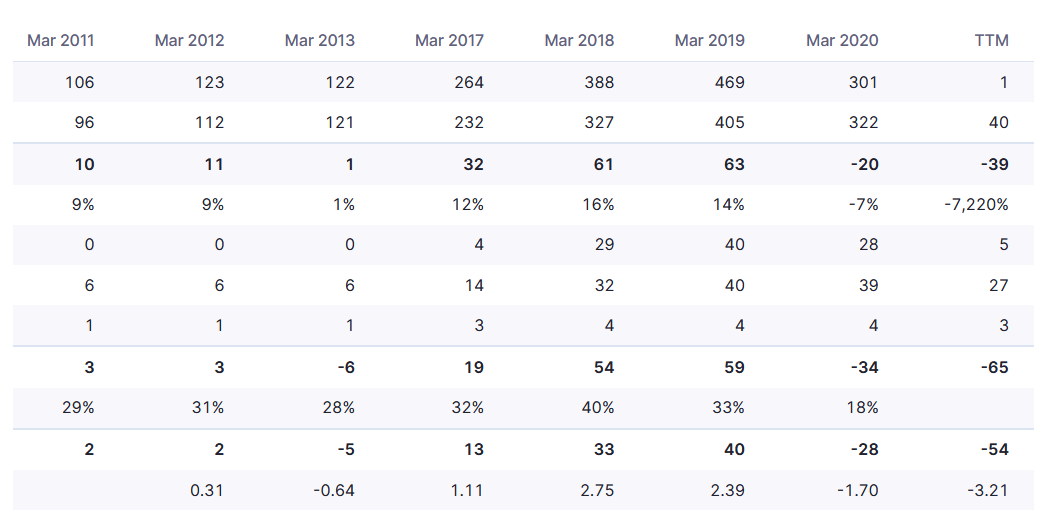

Full incentives will not be easy and will require substantially higher productivity than exhibited currently. Further, manufacturing of electrical goods has not been a terribly profitable activity for PGE (10-year financials attached) with op margin hovering between 5-8%. (10/n)

Assuming it can be meet the targets under the PLI scheme, the company will see a significant boost to the bottomline with the incentives and likely benefit from economies of scale seen in other contract manufacturing companies. (11/n)

To make money you need to deploy money in the first place, though. PG Electroplast does not have leeway on operating metrics to take on much debt. The operations are barely breaking even, at best, after overheads and tax. . (12/n)

Taking advantage of a small window of opportunity requires agile capital. PE funds decide quickly and bring with them other capital like family funds. Preferential allotments to specific investors require a special resolution of the shareholders (>75%), an EGM beckons. (13/n)

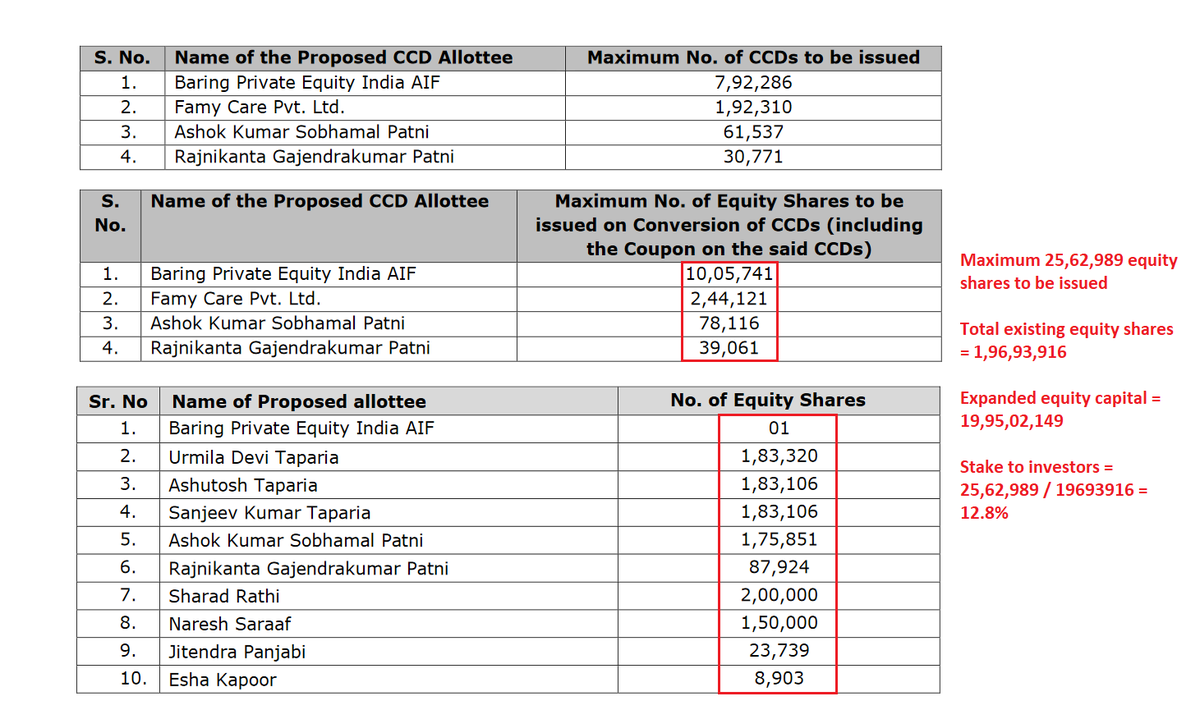

The EGM process is underway at PG Electroplast. The terms of the allotment including price, quantity and the conditions attached to the securities are required to be disclosed. In this instance, the investors are being issued a mix of equity shares and CCDs. (14/n)

Equity shares is simple enough, but what are CCDs? CCDs are hybrid instruments that start as debt and get converted into equity shares. At the time of issuance, the terms including price, the point of conversion and the interest rate are decided upfront. (15/n)

We can see this in the disclosure on 27 May 2021. CCDs are being allotted at a price of INR 337. Convertible within 18 months (at the end or earlier if the holder chooses) at a price of INR 337 per CCD. Till then, the holder gets 17.96% p.a. interest on the CCDs. (16/n)

It is interesting to note that while the interest is 18%, it may not be paid out at all. The cumulative value of the CCDs is the face value of debentures PLUS the accrued interest. Accordingly, the quantity of shares to be issued is the cumulative value divided by INR 337. (17/n)

Essentially, the investors invest into 10,76,904 CCDs at INR 337 each totaling INR 36.29 crore. However, the maximum consideration is stated to be INR 46.06 crore. The differential of INR 9.77 crore is the 17.96% p.a. interest for 18 months. (18/n)

Assuming conversion at 18 months, INR 9.77 crore interest translates into approximately 290,000 extra equity shares for investors. Instead of 10,76,904 equity shares for INR 36.29 crore invested, investors get 13,67,039 equity shares worth INR 46.06 crore (27% increase). (19/n)

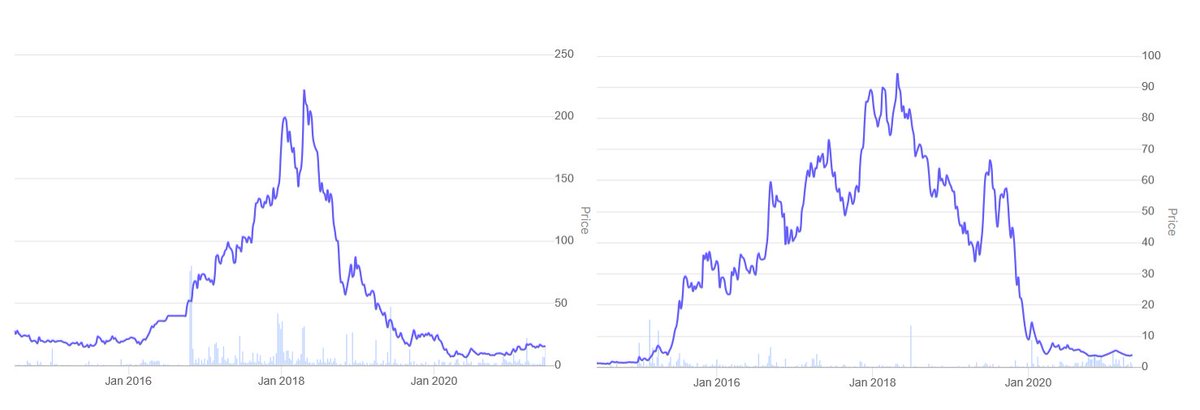

The 'interest' part here is just a mechanism for the PE Investor to get 27% more shares than it would get converting at market price at the time of investment. If you see the price chart, PG Electroplast was also trading around INR 340 at the time of the announcement. (20/n)

This is essentially the premium a PE investor demands for putting in the money before the magic is underway. Said another way, if the market price is still 337 per share in 18 months, the PE investor can book 27% returns if it sells immediately upon conversion. (21/n)

If the market price is higher than INR 337, the PE investor makes a killing with the 27% extra shares and fixed conversion price. It is relevant to highlight that the PE investor can always take 18% interest in cash if there is a material change in the circumstances. (22/n)

To visualize, see the attached Excel calculation on the broad range of outcomes for the CCDs. Essentially, the CCD holders can break even on conversion at market prices as low as INR 245 if they take out interest in cash, or INR 265 without taking out interest! CMP = 408. (23/n)

The CCD route has benefits for both parties – company gets cash upfront and can deduct the accrued interest from its P&L statement and capitalize it without cash outflow. The CCD holders hedge their risk and get a discount while the funds are being deployed by the company. (24/n)

It is telling that while all investors are taking a mix of CCDs and equity shares in the beginning, only Baring Private Equity is putting its entire investment as CCDs, w/ only 1 equity share alloted. Baring PE hedged its risk upfront, in line with its customary PE model. (25/n)

Normally such deals in the private space will result in the investors taking preferential rights to recoup their investment, even with only 10% stake in the company. However, in the listed space, this would be difficult to carry out. (26/n)

So, the PE investor agrees to a discounted issuance (accrued interest mechanism) and gets assured liquidity to exit the investment through the stock exchanges. It is essentially a hedged bet that the market will ascribe a much higher value to the company in the future. (27/n)

From the above it may seem like the PE investor is getting a great deal, especially the CCD holders. However, there is many a slip between the cup and the lip. As stated before, the incentives will flow after a while and will need pinpoint execution and actual sales. (28/n)

Contract manufacturing is nascent in India and very few companies (especially listed ones) have achieved the scale to make stable returns on investment. However, this is the entire theme of the PLI schemes and anyone who can execute will establish themselves for years. (29/n)

5% incentive will not transform PGE, it will only make the operations somewhat more profitable. It is only a part of a vision, the company will still be subject to commercial factors such as customer demand, competition and economic conditions. (30/n)

Many may ask whether this transaction good or bad for shareholders? It is a matter of perspective and is a determination that differs from company to company. Given the risk involved, existing shareholders are typically glad to let someone else put in the money. (31/n)

In this case, Baring PE is that someone else. Though there are other investors too, Baring PE was the lead investor here, amply evident from it having a lion’s share of the CCDs and favourable terms, and it possibly syndicated the rest of the investors into the deal too. (32/n)

Public shareholders are generally happy diluting to experienced investors with deep pockets, as it signals the attractiveness of the investment thesis. It attracts a whole flurry of new public shareholders, as evident from the sharp rise in price in the last 2 weeks. (33/n)

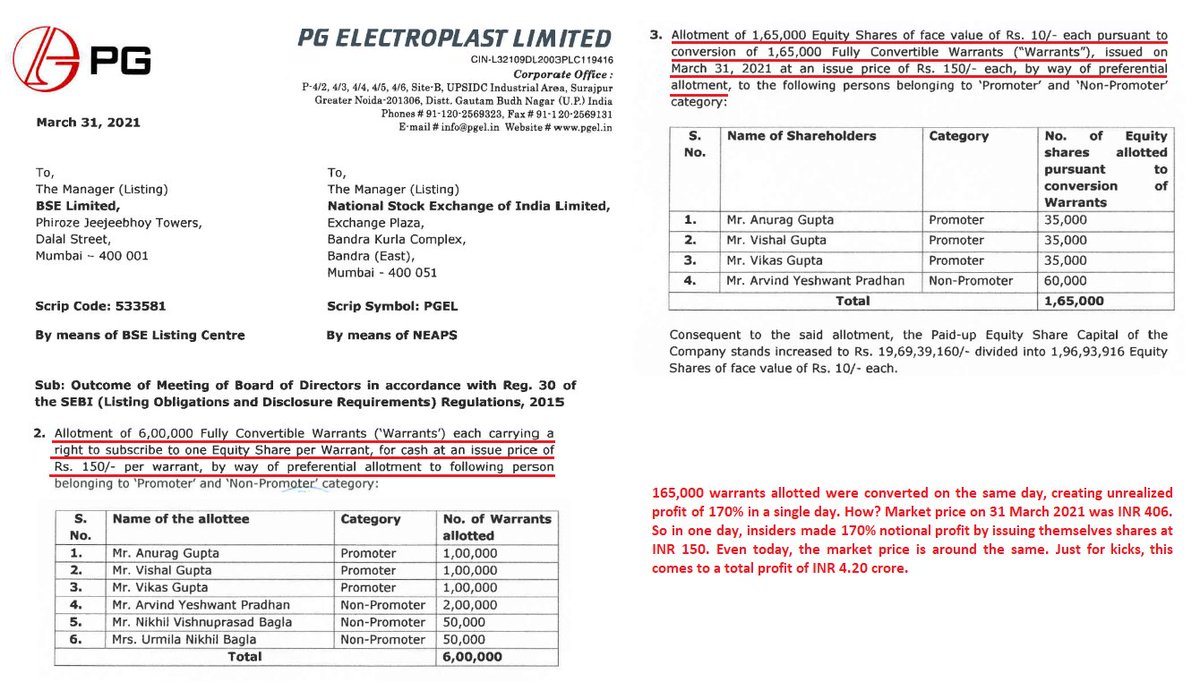

It is worthwhile to point out that the promoters issued and converted warrants to themselves at INR 150 per share in March 2021; less half the INR 337 price paid by the new investors and less than half the price prevailing on 31 March 2021. (34/n)

The ethics are debatable. If these talks were already underway in March 2021, the warrant issuance is opportunism. If promoters have cash to invest, perhaps they should join the new investors at similar terms. Issuing warrants at 60% discount, seems like a cash grab. (35/n)

Overall, earning performance will hinge on execution, especially with a capex plan expected to add INR 1500 crore sales over 5 years. Other contract manufacturers like Amber Enterprises and Dixon Technologies have done well on execution and scale of operations. (36/n)

A large part of the reason I wrote this thread is to contextualize. To understand what promoters and PE investors are betting on and how they're hedging their risk. Once you understand this, you can form your own considered view on the investment thesis. (37/n)

As always, this is just a series of explanations and observations. Not intended to be interpreted as a recommendation to buy or sell or take any action. (38/n)

P.S. Many ask how I find these corporate events. I made my own screener (@bsescreener) with

@ghanishtnagpal for stock market announcements and these corporate actions show up frequently there. I first caught this 2 weeks ago and then again 4 days ago. (39/n)

Read my last thread on bonus debentures by Britannia here:

https://t.co/2taUEn4V2G