1/x The market continues to try & shake out weak hands from overextended positioning by both HF & Retail...After a strong Vanna run up overnight, as expected, retail exuberance exploded on the open in the form of retail call buying, this fragility, paired w/a)Mean reverting flows

More from Cem Karsan 🥐

1/x Vanna joined the wheel of fortune on this day in 1982,& 38 years later she’s stronger than ever...Friday’s into the Mon of qrtrly OpEx in particular aren’t a time to trifle w/her...As called for, the market continues to try & shake out weak hands from overextended positioning

2/x by both HF & Retail, but ultimately these moves are no match for our fair lady’s charming flows during this window, & should continue to support this market through 12/16 w/ qrtrly Vixperation & the Fed upon us....As I highlighted Fri, the minor correction in price/time that

3/x we got down to the 20 day, w/precise technical support at that level, paired w/ increasingly positive Dark Pool (DIX) demand was a textbook buy signal, given the timing...Despite all of this, the real story is not these positive flows nearly as much as the continued reflexive

4/x IVol compression...This is the holiday gift that keeps on giving. Along w/ continued targeted short Vol, massive calendar expansion & dispersion opportunities continue to print $ with VRP >94th % of occurrences & post 1/8 Vol still at a floor... This $ train doesn’t show any

5/x sign of stopping yet, as I expect Ivol oversupply should continue to be the dominant force through at least 12/16 & once we get through 12/21 without incident, likely beyond...W/ lots of imbedded potential energy still in the VRP to fuel more vanna/charm flows in the month to

\U0001f4faOn December 13, 1982, Vanna White joined @WheelofFortune pic.twitter.com/rzrPcBTI59

— RetroNewsNow (@RetroNewsNow) December 13, 2020

2/x by both HF & Retail, but ultimately these moves are no match for our fair lady’s charming flows during this window, & should continue to support this market through 12/16 w/ qrtrly Vixperation & the Fed upon us....As I highlighted Fri, the minor correction in price/time that

3/x we got down to the 20 day, w/precise technical support at that level, paired w/ increasingly positive Dark Pool (DIX) demand was a textbook buy signal, given the timing...Despite all of this, the real story is not these positive flows nearly as much as the continued reflexive

4/x IVol compression...This is the holiday gift that keeps on giving. Along w/ continued targeted short Vol, massive calendar expansion & dispersion opportunities continue to print $ with VRP >94th % of occurrences & post 1/8 Vol still at a floor... This $ train doesn’t show any

5/x sign of stopping yet, as I expect Ivol oversupply should continue to be the dominant force through at least 12/16 & once we get through 12/21 without incident, likely beyond...W/ lots of imbedded potential energy still in the VRP to fuel more vanna/charm flows in the month to

1/x As we’ve been calling for since Nov, today we finally got our 2 ‘Georgia Peaches’🍑 precisely on schedule, as we’ve called for since Aug, & the underlying rotation has confirmed now for months, this matters. This is a historic turning point. It matters not only https://t.co/BFxKGrI1Oo

2/x for this year, but for the economic trajectory of America & likely the macroeconomic regime of the developed world for the coming decade. That said, contrary to popular belief, the market does not move based on news in the short term if the positioning doesn’t allow it to.

3/x & our old friend Gary the 🦍 & his sidekick Vanna are positioned to have this market pinned through 1/11. So, as explained ad nauseam, the election news, though fundamentally important, won’t matter to the index itself in the ST. As predicted, the largest moves from the GA

4/x runoff INITIALLY have come from factor rotation. This should continue to be the case, as the street is oversupplied IVol & the index is pinned. This not only allows for idiosyncratic risk moves in constituents, but it actually FORCES extreme noncorrelation & rotation, as we

5/x have witnessed now for the past 2 days. This Vol compression will be increasingly difficult to break free from until 1/11-1/15, but the window of weakness is coming...soon the final hedges from the ‘election hump’ in Nov will expire with the Jan monthly options. Once the

1/x Well you can\u2019t say I didn\u2019t warn you... We\u2019ve been eying that 3770.5 level and the 1/5-1/13 window for many weeks. To get it a day early, @ the lowest edge of the upper range, tells me that there\u2019s understandable concern over the impending outcome of the runoff. As I\u2019ve said https://t.co/BxG2DzdXqt pic.twitter.com/ki4sYprwIH

— Cem Karsan \U0001f950 (@jam_croissant) January 5, 2021

2/x for this year, but for the economic trajectory of America & likely the macroeconomic regime of the developed world for the coming decade. That said, contrary to popular belief, the market does not move based on news in the short term if the positioning doesn’t allow it to.

3/x & our old friend Gary the 🦍 & his sidekick Vanna are positioned to have this market pinned through 1/11. So, as explained ad nauseam, the election news, though fundamentally important, won’t matter to the index itself in the ST. As predicted, the largest moves from the GA

4/x runoff INITIALLY have come from factor rotation. This should continue to be the case, as the street is oversupplied IVol & the index is pinned. This not only allows for idiosyncratic risk moves in constituents, but it actually FORCES extreme noncorrelation & rotation, as we

5/x have witnessed now for the past 2 days. This Vol compression will be increasingly difficult to break free from until 1/11-1/15, but the window of weakness is coming...soon the final hedges from the ‘election hump’ in Nov will expire with the Jan monthly options. Once the

More from Economy

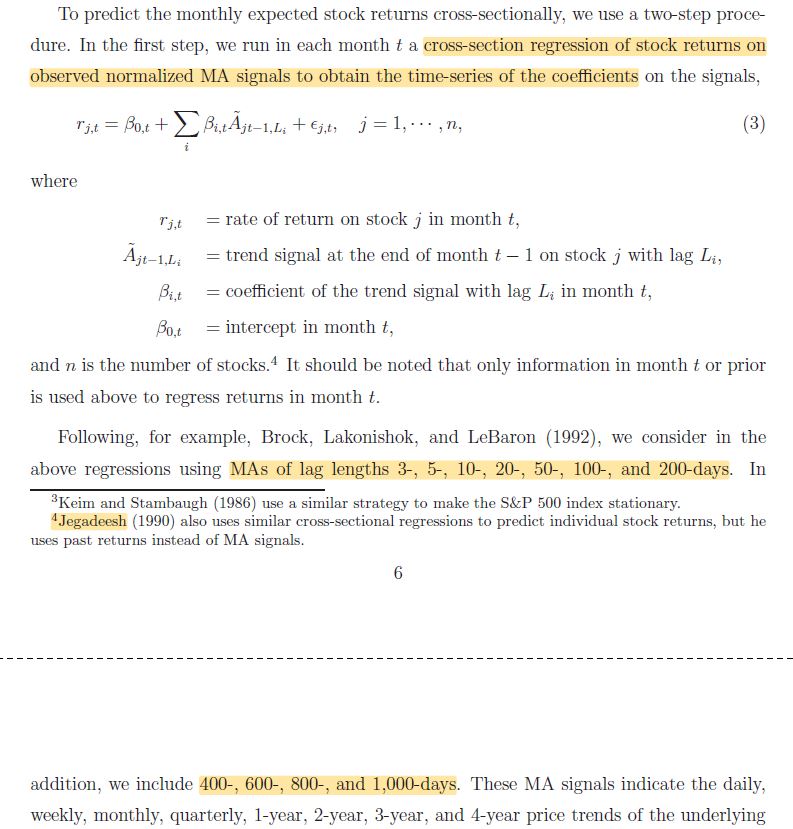

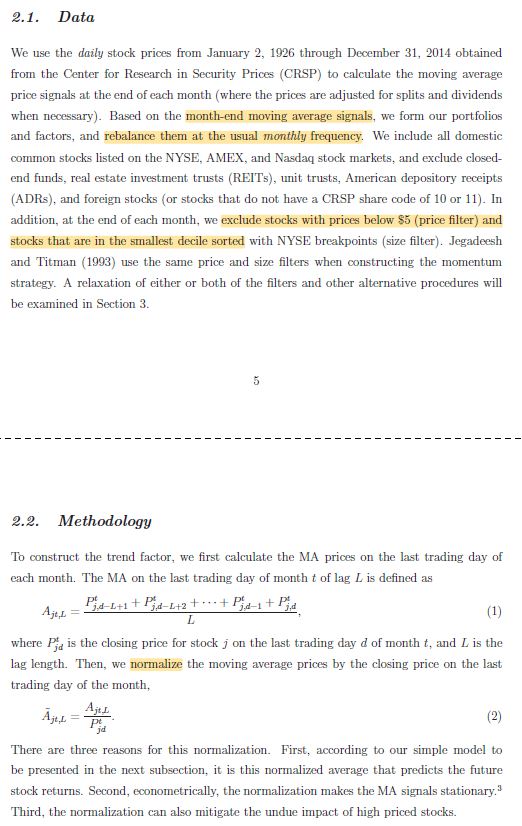

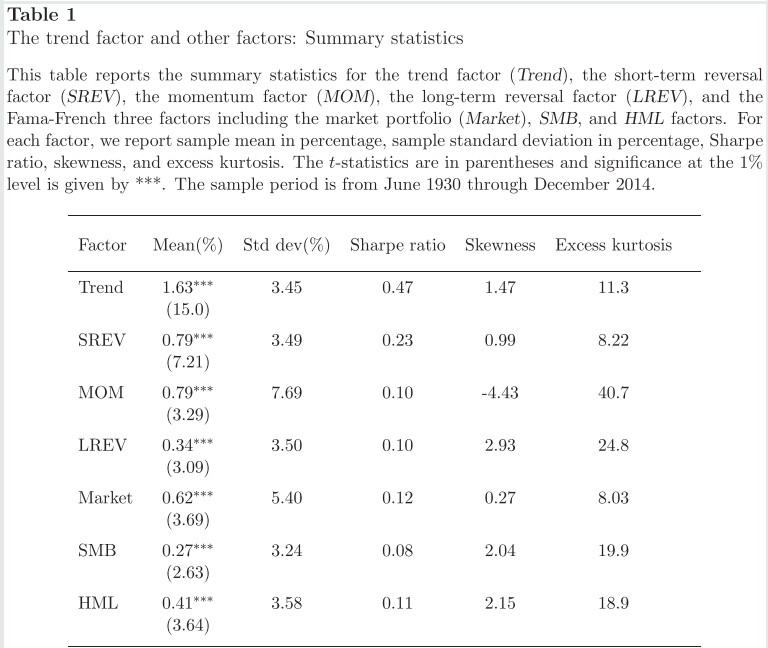

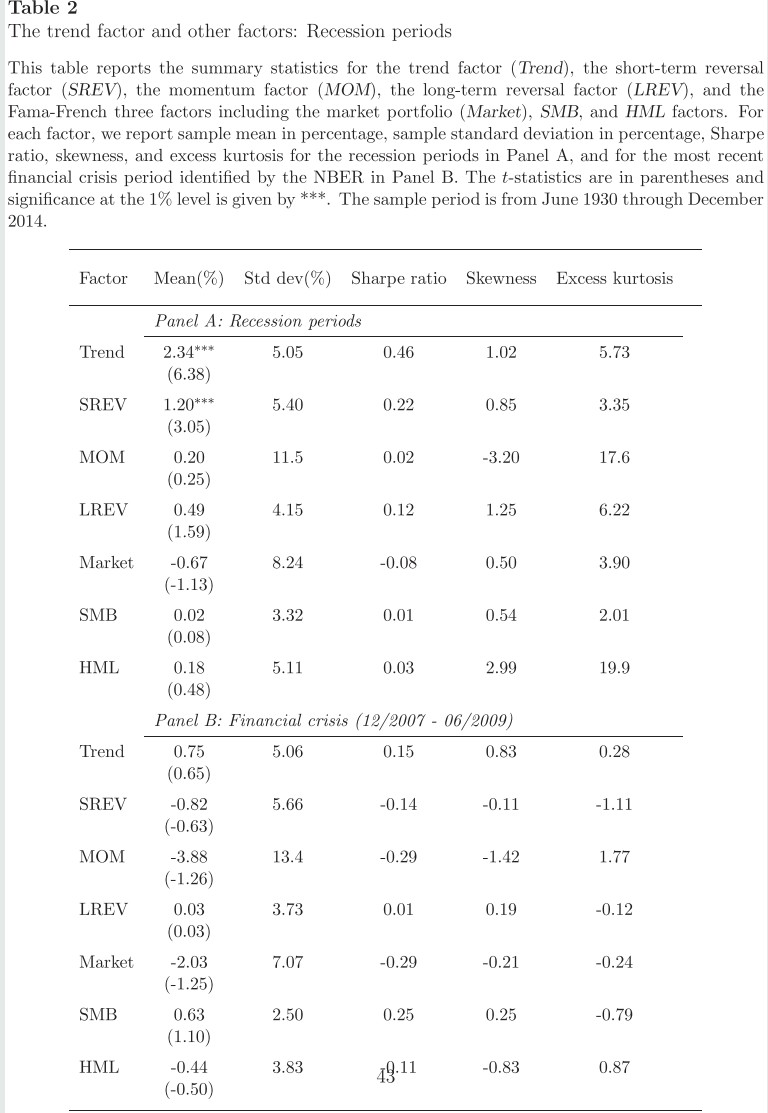

1/ Trend Factor: Any Economic Gains from Using Information over Investment Horizons? (Han, Zhou, Zhu)

"A trend factor using multiple time lengths outperforms ST reversal, momentum, and LT reversal, which are based on the three price trends separately."

https://t.co/udkvsdw2Lz

2/ This resembles combining multiple measures of ST reversal, momentum, and LT reversal (forecasts determined by walking forward rather than using signs from the full sample).

Unlike normal moving average signals, these are *cross-sectional.* More below:

https://t.co/wkIFLg9jtK

3/ Unsurprisingly, the Trend factor formed by this approach outperforms benchmarks in terms of both Sharpe ratio and tail metrics. It's combining momentum with two factors that are negatively correlated to it AND using multiple specifications.

More here:

https://t.co/x8Tloz3iyL

4/ "Average return and volatility of the trend factor are both higher in recession periods. However, the Sharpe ratio is virtually the same.

"Interestingly, all of the factors still have positive average returns.

"Momentum experiences the greatest increase in volatility."

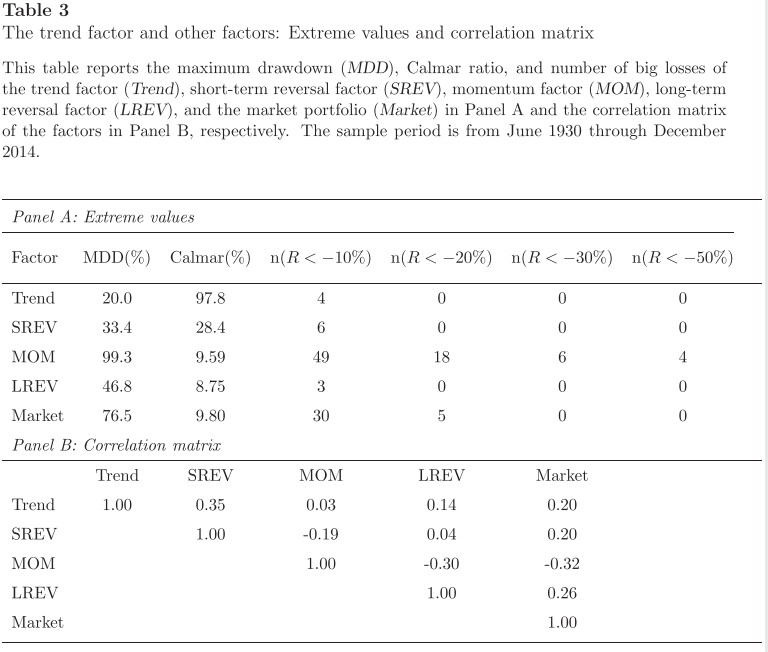

5/ "In terms of maximum drawdown and the Calmar ratio, the trend factor performs the best.

"The trend factor is correlated with the short-term reversal factor (35%), long-term reversal factor (14%), and the market (20%) but is virtually uncorrelated with the momentum factor."

"A trend factor using multiple time lengths outperforms ST reversal, momentum, and LT reversal, which are based on the three price trends separately."

https://t.co/udkvsdw2Lz

2/ This resembles combining multiple measures of ST reversal, momentum, and LT reversal (forecasts determined by walking forward rather than using signs from the full sample).

Unlike normal moving average signals, these are *cross-sectional.* More below:

https://t.co/wkIFLg9jtK

1/ Cross-Sectional and Time-Series Tests of Return Predictability: What Is the Difference? (Goyal, Jegadeesh)

— Darren \U0001f95a (@ReformedTrader) June 18, 2019

"The difference between the performances of TS and CS strategies is largely due to a time-varying net-long investment in risky assets."https://t.co/CSIn3ujN2R pic.twitter.com/XHnVmIart4

3/ Unsurprisingly, the Trend factor formed by this approach outperforms benchmarks in terms of both Sharpe ratio and tail metrics. It's combining momentum with two factors that are negatively correlated to it AND using multiple specifications.

More here:

https://t.co/x8Tloz3iyL

1/ An Executive Summary (in Tweet form) of our new paper

— Adam Butler (@GestaltU) March 27, 2019

Dual Momentum \u2013 A Craftsman\u2019s Perspective

Download here: https://t.co/Y9GlGNohBg

Everything that follows in this thread is based on HYPOTHETICAL AND SIMULATED RESULTS. pic.twitter.com/9m5YJnTdtq

4/ "Average return and volatility of the trend factor are both higher in recession periods. However, the Sharpe ratio is virtually the same.

"Interestingly, all of the factors still have positive average returns.

"Momentum experiences the greatest increase in volatility."

5/ "In terms of maximum drawdown and the Calmar ratio, the trend factor performs the best.

"The trend factor is correlated with the short-term reversal factor (35%), long-term reversal factor (14%), and the market (20%) but is virtually uncorrelated with the momentum factor."

It's always been detached, and it's always made the real economy worse.

[THREAD] 1/10

What is profit? It's excess labor.

You and your coworkers make a chair. Your boss sells that chair for more than he pays for the production of that chair and pockets the extra money.

So he pays you less than what he should and calls the unpaid labor he took "profit." 2/10

Well, the stock market adds a layer to that.

So now, when you work, it isn't just your boss that is siphoning off your excess labor but it is also all the shareholders.

There's a whole class of people who now rely on you to produce those chairs without fair compensation. 3/10

And in order to support these people, you and your coworkers need to up your productivity. More hours etc.

But Wall Street demands endless growth in order to keep the game going, so that's not enough.

So as your productivity increases, your relative wages suffer. 4/10

Not because the goods don't have value or because your labor is worth less. Often it's actually worth more because you've had to become incredibly productive in order to keep your job.

No, your wages suffer because there are so many people who need to profit from your work. 5/10

[THREAD] 1/10

I know people think this is fun but -- why do we have a stock market? So productive firms can raise capital to do useful things. Detaching stock price from fundamental value (Gamestop is now worth almost as much as Best Buy) makes the markets serve the real economy worse.

— Josh Barro (@jbarro) January 27, 2021

What is profit? It's excess labor.

You and your coworkers make a chair. Your boss sells that chair for more than he pays for the production of that chair and pockets the extra money.

So he pays you less than what he should and calls the unpaid labor he took "profit." 2/10

Well, the stock market adds a layer to that.

So now, when you work, it isn't just your boss that is siphoning off your excess labor but it is also all the shareholders.

There's a whole class of people who now rely on you to produce those chairs without fair compensation. 3/10

And in order to support these people, you and your coworkers need to up your productivity. More hours etc.

But Wall Street demands endless growth in order to keep the game going, so that's not enough.

So as your productivity increases, your relative wages suffer. 4/10

Not because the goods don't have value or because your labor is worth less. Often it's actually worth more because you've had to become incredibly productive in order to keep your job.

No, your wages suffer because there are so many people who need to profit from your work. 5/10