The existence of stablecoins does not prevent consumers from using any other traditional payment, savings or credit offerings

The #STABLEAct is a confused attempt at regulating perceived harms that are not actually caused by the technology, but are, ironically, inherent in the existing financial system that cryptocurrencies are designed to replace

👇🏽

The existence of stablecoins does not prevent consumers from using any other traditional payment, savings or credit offerings

This happens when banks make arbitrary and opaque risk decisions that are in turn based on cumbersome regulations which deputize banks to do the government’s job

1. Stablecoin issuers could take advantage of low income consumers

2. Stablecoins are an ‘outsourced issuance’ of US dollars

3. Stablecoins pose market, liquidity, and credit risk

But all of these concerns are misplaced👇🏽

https://t.co/g997ym8zCV

This is the opposite of stablecoins like USDC, which are fully collateralized and don't charge interest or fees

This objective does not justify regulating the issuance or transactional use of stablecoins

They are, at most, the issuance of a promise to redeem 1 stablecoin for 1 US Dollar, the same way as a check or money order

This issuance is already regulated under state money transmission laws

Perhaps they refer to the risk that stablecoins could become 'too big to fail' or somehow cause a 2008 style financial crisis, which of course is absurd...

And again, there are existing laws (state money transmission) which require issuers of stablecoins to have fully collateralized reserves with a 1:1 backing.

More from Crypto

1/ Welcome to #DeFi Wednesday.

Let's talk about how interest-bearing cash on a blockchain is going to revolutionise boring corporate treasury management that concerns every company is is a larger business than all crypto trading in the world.

Enter the thread

👇👇👇

2/ Blockchain community is often seen as toxic maxis and redditors who shill other their weekly favourite shitcoin in the hope of getting Lambo.

Sometimes we also do things that progress humanity towards the better future and interest-bearing cash is one of those things.

3/ Less chad and more things that actually matter:

My incomplete theory of interest-bearing cash is also available also as a blog post:

https://t.co/uiG0fZiVyu

It is 15 pages. Pick your slow poison or die fast by continue reading here.

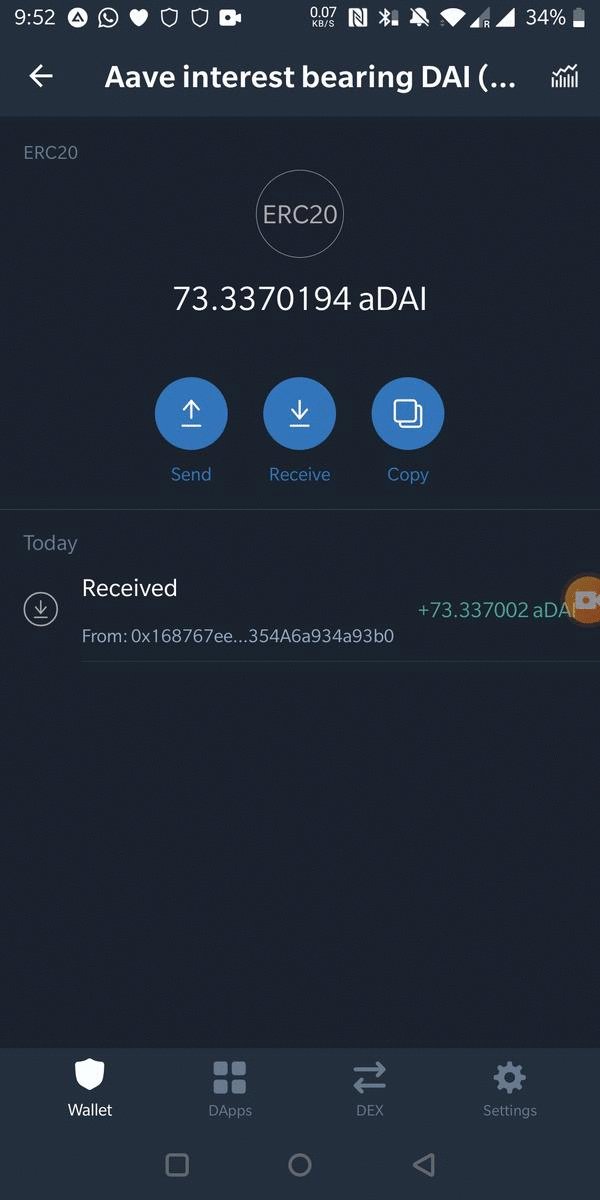

4/ First time in the history we have an ability to create interest-bearing cash-like instruments.

Interest-bearing cash ticks up dollar (euro) balance real-time in your wallet.

Here is a demonstration using @aaveaave aDAI, based on @makerdao DAI, and @TrustWalletApp

5/ Interest-bearing cash is not like your bank's saving account. Your money in a bank is not yours, but bank's. There are some flaws in the current banking system causing a headache for Chief Financial Officers (CFOs)

Let's talk about how interest-bearing cash on a blockchain is going to revolutionise boring corporate treasury management that concerns every company is is a larger business than all crypto trading in the world.

Enter the thread

👇👇👇

2/ Blockchain community is often seen as toxic maxis and redditors who shill other their weekly favourite shitcoin in the hope of getting Lambo.

Sometimes we also do things that progress humanity towards the better future and interest-bearing cash is one of those things.

3/ Less chad and more things that actually matter:

My incomplete theory of interest-bearing cash is also available also as a blog post:

https://t.co/uiG0fZiVyu

It is 15 pages. Pick your slow poison or die fast by continue reading here.

4/ First time in the history we have an ability to create interest-bearing cash-like instruments.

Interest-bearing cash ticks up dollar (euro) balance real-time in your wallet.

Here is a demonstration using @aaveaave aDAI, based on @makerdao DAI, and @TrustWalletApp

5/ Interest-bearing cash is not like your bank's saving account. Your money in a bank is not yours, but bank's. There are some flaws in the current banking system causing a headache for Chief Financial Officers (CFOs)

You May Also Like

So it's now October 10, 2018 and....Rod Rosenstein is STILL not fired.

He's STILL in charge of the Mueller investigation.

He's STILL refusing to hand over the McCabe memos.

He's STILL holding up the declassification of the #SpyGate documents & their release to the public.

I love a good cover story.......

The guy had a face-to-face with El Grande Trumpo himself on Air Force One just 2 days ago. Inside just about the most secure SCIF in the world.

And Trump came out of AF1 and gave ol' Rod a big thumbs up!

And so we're right back to 'that dirty rat Rosenstein!' 2 days later.

At this point it's clear some members of Congress are either in on this and helping the cover story or they haven't got a clue and are out in the cold.

Note the conflicting stories about 'Rosenstein cancelled meeting with Congress on Oct 11!"

First, rumors surfaced of a scheduled meeting on Oct. 11 between Rosenstein & members of Congress, and Rosenstein just cancelled it.

He's STILL in charge of the Mueller investigation.

He's STILL refusing to hand over the McCabe memos.

He's STILL holding up the declassification of the #SpyGate documents & their release to the public.

I love a good cover story.......

The guy had a face-to-face with El Grande Trumpo himself on Air Force One just 2 days ago. Inside just about the most secure SCIF in the world.

And Trump came out of AF1 and gave ol' Rod a big thumbs up!

And so we're right back to 'that dirty rat Rosenstein!' 2 days later.

At this point it's clear some members of Congress are either in on this and helping the cover story or they haven't got a clue and are out in the cold.

Note the conflicting stories about 'Rosenstein cancelled meeting with Congress on Oct 11!"

First, rumors surfaced of a scheduled meeting on Oct. 11 between Rosenstein & members of Congress, and Rosenstein just cancelled it.

Rep. Andy Biggs and Rep. Matt Gaetz say DAG Rod Rosenstein cancelled an Oct. 11 appearance before the judiciary and oversight committees. They are now calling for a subpoena. pic.twitter.com/TknVHKjXtd

— Ivan Pentchoukov \U0001f1fa\U0001f1f8 (@IvanPentchoukov) October 10, 2018