@HDFCLIFE #Q3marketupdates #Q3investorpresentations

Mkt share up 214 bps to 16.4%

NBM at 25.6%

8% Individual WRP growth compared to private industry de-growth of 6%

25.6% New Business Margin on the back of growth, balanced product mix

17% growth in Protection (Indl) and 42% growth in Annuity in APE terms

22% growth in renewal premium with stable persistency

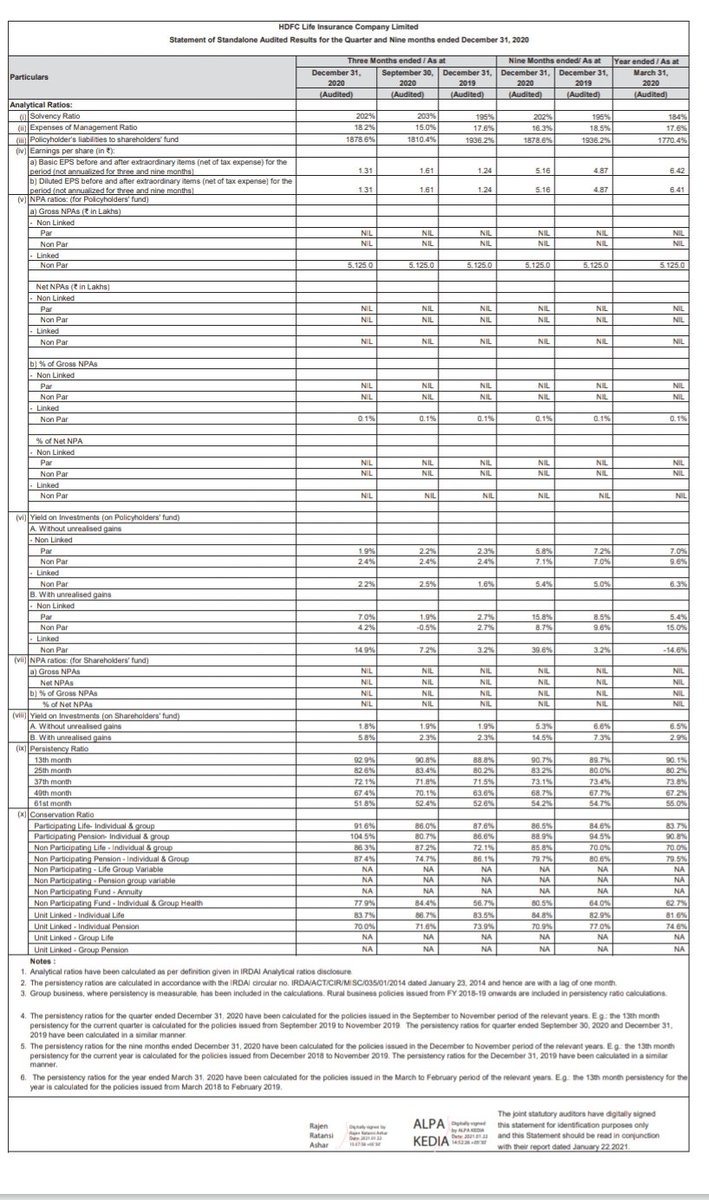

PAT of Rs 1,042 Cr, with growth of 6%

Solvency healthy at 202%

Pvt mkt share rank up to 2,gain 214 bps 14.3 to 16.4%

Balanced product mix %

Savings 35

Non participating savings 30

Ulips 23

Protection 7

Annuity 5

Distribution 300+ partners

AUM 31Dec 20

1.7 lkh cr

Debt:equity mix 64:36

98% debt in Gsecs & AAA

Renewal premium growth 22%

NBM 25.6%

PAT 10.4 bn,up 6%

Solvency ratio 202%

42 % growth in annuity business

NBM %

2019 24.6

2020 25.9

9 months fy21 25.6

Strong partner ships

Hdfc bank ,Yes ,RBL , pnb housing ,Idfc 1st

etc

Sustained growth in Individual protection %

2018 2.5

9mnth fy21 3

NPS - #1 with AUM 139 bn amongst pvt players ,strong growth AUM 9mnths 81%

26000 lives covered in 9mnths Fy21

5 building blocks

Insta suite

InstaInsure

Online payments & services

AI ,Big data ,Cloud

Life 99