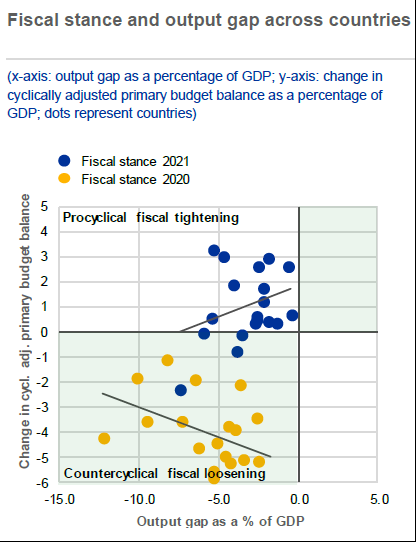

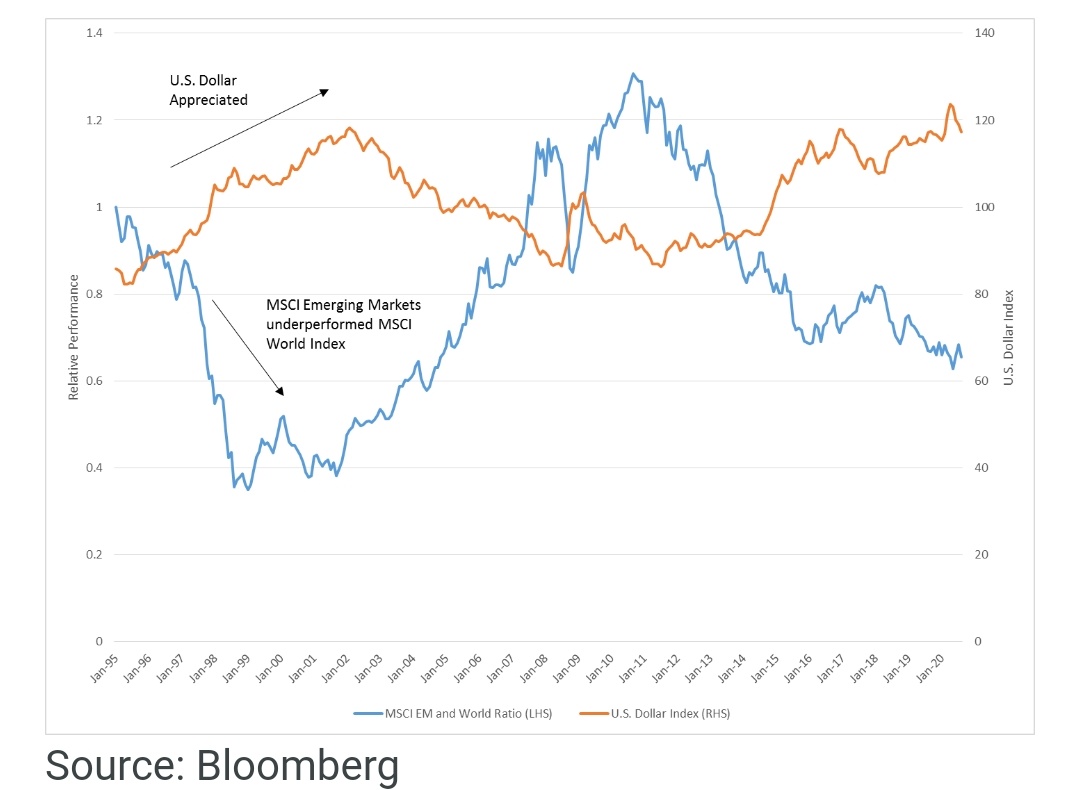

The excellent ECB Financial Stability Review, https://t.co/k8HcqpryDF illustrates well the 2 main risks I see for the EA economy next year: possible insufficient fiscal stimulus and weakening of bank credit supply. The FSR mentions “a slightly tighter fiscal stance" in 2021 1/

More from Finance

You May Also Like

First thread of the year because I have time during MCO. As requested, a thread on the gods and spirits of Malay folk religion. Some are indigenous, some are of Indian origin, some have Islamic

Before I begin, it might be worth explaining the Malay conception of the spirit world. At its deepest level, Malay religious belief is animist. All living beings and even certain objects are said to have a soul. Natural phenomena are either controlled by or personified as spirits

Although these beings had to be respected, not all of them were powerful enough to be considered gods. Offerings would be made to the spirits that had greater influence on human life. Spells and incantations would invoke their

Two known examples of such elemental spirits that had god-like status are Raja Angin (king of the wind) and Mambang Tali Arus (spirit of river currents). There were undoubtedly many more which have been lost to time

Contact with ancient India brought the influence of Hinduism and Buddhism to SEA. What we now call Hinduism similarly developed in India out of native animism and the more formal Vedic tradition. This can be seen in the multitude of sacred animals and location-specific Hindu gods

i wonder if you can make a thread bout witchcraft in malaysia.. or list of our own local gods/deites..

— r a y a \U0001f319 (@lcvelylilith) February 20, 2020

Before I begin, it might be worth explaining the Malay conception of the spirit world. At its deepest level, Malay religious belief is animist. All living beings and even certain objects are said to have a soul. Natural phenomena are either controlled by or personified as spirits

Although these beings had to be respected, not all of them were powerful enough to be considered gods. Offerings would be made to the spirits that had greater influence on human life. Spells and incantations would invoke their

Animist ceremonies of a religious or magical nature were normally held for the purpose of divination or making a request. This would either be done at a keramat or at a shrine similar to the Thai spirit houses or Chinese roadside shrines pic.twitter.com/I1hliyi0x3

— \u2745\u1710\u170b\u1713\u170e (@uglyluhan) June 16, 2019

Two known examples of such elemental spirits that had god-like status are Raja Angin (king of the wind) and Mambang Tali Arus (spirit of river currents). There were undoubtedly many more which have been lost to time

Contact with ancient India brought the influence of Hinduism and Buddhism to SEA. What we now call Hinduism similarly developed in India out of native animism and the more formal Vedic tradition. This can be seen in the multitude of sacred animals and location-specific Hindu gods