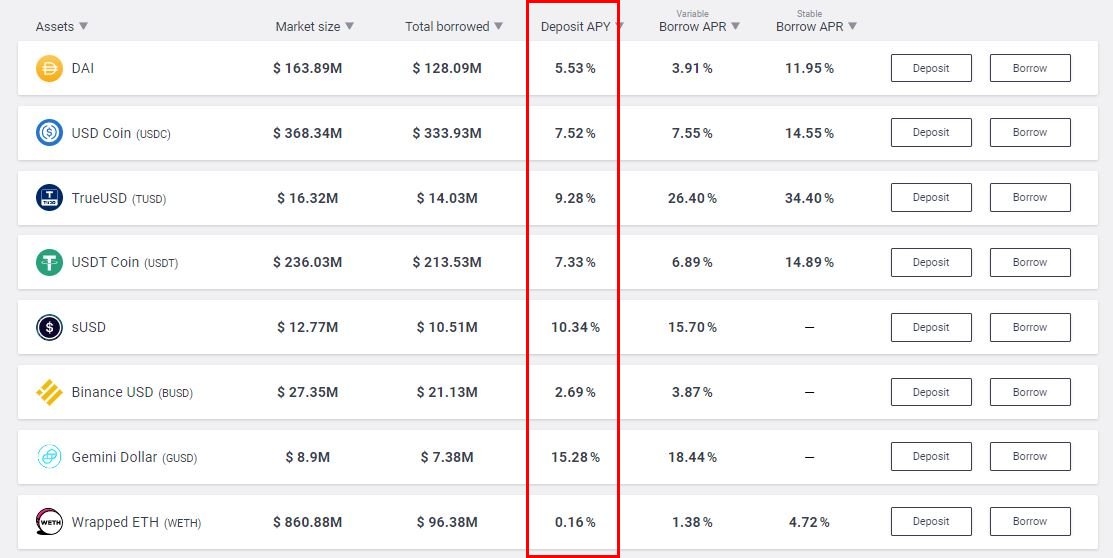

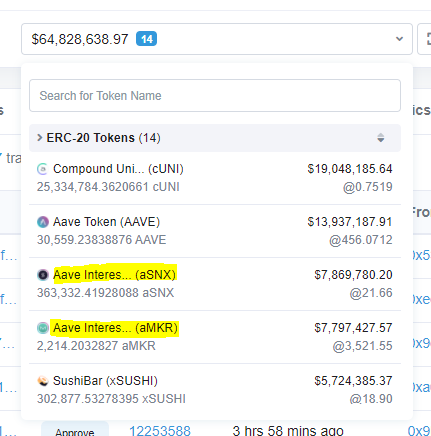

Aave also allows those will idle assets to earn a relatively safe return on capital from lenders, whose rates are determined by a curve.

We're in the phase of the market where there's a lot of retail inbounds but not enough education about the Ethereum ecosystem and DeFi.

So, let's break down the basics of some of the top protocols.

First on deck: Aave (@AaveAave), an Ethereum-based money market protocol.

A 🧵

Aave also allows those will idle assets to earn a relatively safe return on capital from lenders, whose rates are determined by a curve.

Users would hold BTC, ETH, and other assets (including many ERC-20 tokens) with no expectation of a native yield or dividends.

ETH, for instance, was long just an asset for transaction fees, as was Bitcoin.

Users can deposit a variety of assets as collateral, then use that collateral as ammo to borrow other assets to be used in DeFi or beyond.

Loans are *overcollateralized*.

1. Those looking for steady, relatively safe yield on idle assets.

2. Those that want to leverage their assets by borrowing against their holdings, then trading and spending the loan to achieve utility beyond the rate they pay.

- Find idle assets that can be lent out on Aave

- Deposit said assets

- Earn a per-block, pro-rata interest paid for by those that borrow your assets (assets are pooled, then used) from the protocol

- Find inactive, useless asset

- Deposit it into Aave

- Enable it as collateral

- Borrow desired assets from protocol

- Use borrowed assets for trading, yield farming, spending, etc.

Shorting:

A user can borrow an asset from Aave, sell it, buy it back when the price is lower, then pocket the delta.

This works because the loan is denominated in the asset(s) borrowed.

ETH natively does not produce yield.

It can be used as collateral to borrow assets that *can* earn yield.

Assuming you can earn 15% on USDC and borrow @ 5%, borrowing USDC at a 200% collat. ratio will allow for an effective yield of 5% on ETH.

Say a user is holding Wrapped Bitcoin and wants something on-chain or IRL, though doesn't want to get rid of their WBTC exposure.

A user can collateralize their WBTC, buy what they want, then pay back the loan with income or other assets to reclaim their WBTC.

Aave pioneered flash loans, a concept where anyone can borrow any amount of capital within a single block for a number of use cases.

Did a thread here in the past.

https://t.co/FRn5Pj2TFk

If you've been following DeFi or Ethereum over the past few months, you've likely heard the term "flash loan" mentioned again and again.

— Nick Chong (@n2ckchong) October 29, 2020

This new DeFi primitive has been at the core of a number of economic exploits and arbitrages.

A thread on the basics of flash loans - \U0001f447 pic.twitter.com/uOQC2tzlYl

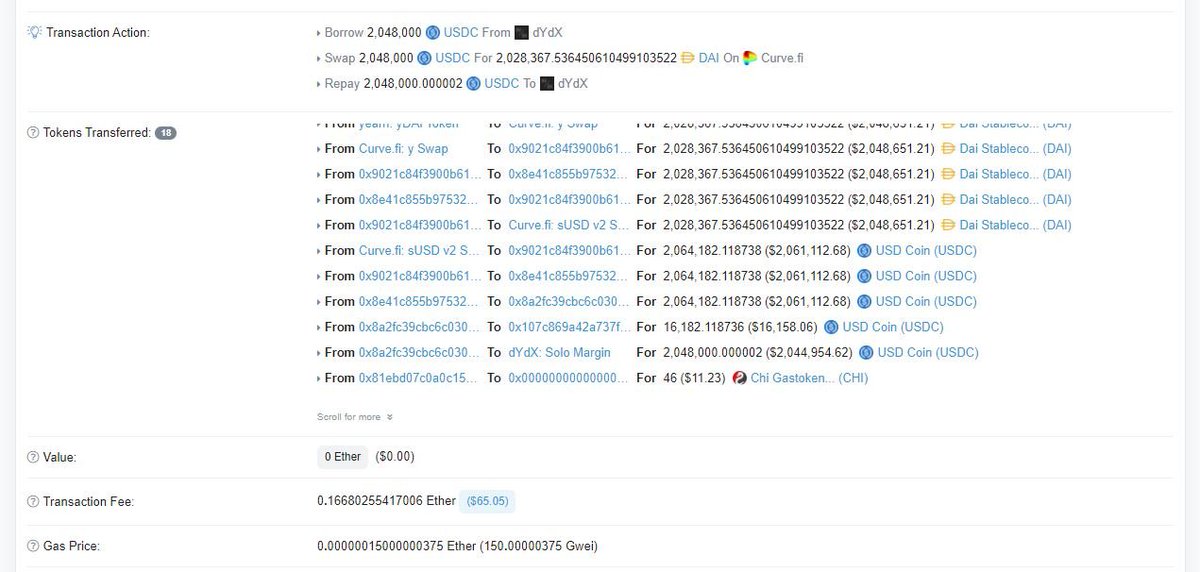

- A user borrowed 2,048,000 USDC from dYdX

- Traded that USDC for 2,028,367 DAI in Curve's Y pool

- Traded that DAI for 2,064,182 USDC in Curve's sUSD pool

- Paid dYdX back + 2 wei

All in one block...

Profit: 16,182 USDC

Cost: $60 in gas

I'll cover:

- Interest rates

- Terms

- Liquidations

- aTokens

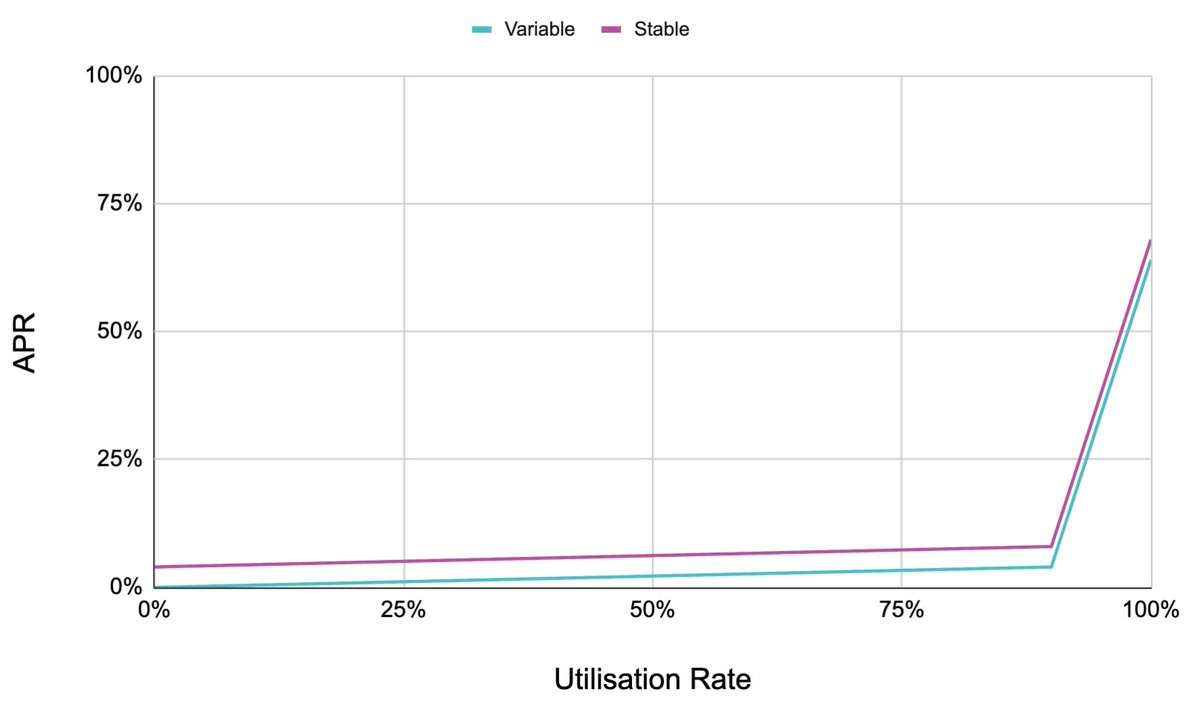

The more an asset is utilized, the higher the rate lenders earn and borrowers pay.

The borrow rate is always above the deposit rate.

Here's the borrow rate model for USDC / USDT.

To mitigate unexpected spikes in utilization affecting the rate one pays on their loan, users can lock in a fixed rate, so they can manage risk properly.

This rate can readjust based on market conditions.

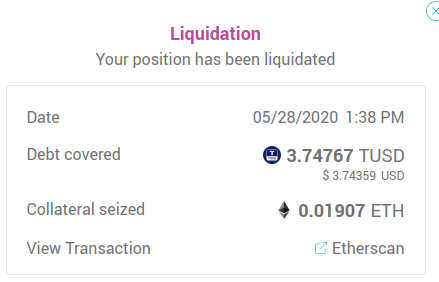

Aave has a number of loan terms that dictate how much one can borrow, at what point they are liquidated, and how much they pay when they are liquidated.

These terms are determined by a risk team, who assess market conditions to minimize risk to protocol collateral.

Unlike traditional loans, Aave loans are liquidated autonomously when a user's loan-to-value ratio falls below certain values.

A large enough drop in the value of one's collateral will allow users to bid the collateral, sell it, then pocket a bonus.

aTokens are yield-bearing assets that accrue interest in real time, allowing one to watch their deposited assets grow by block.

It can be used by other developers to build interesting applications and use cases.

For instance...

@APWineFinance: APWine allows users to trade unrealized yield

etc.

aTokens, flash loans, etc. can all be used in tandem with other contracts to create use cases.

More from Crypto

0/ The Great Crypto Reversal

Key difference between the '17 and roaring 20s in crypto is that back then everyone was aping a16z and Naval.

Today everyone apes 3AC wanting to be the next Degen.

'17 was an idealistic *saving the world* kind of thing

20s is *me against the world*

1/ The financialization of crypto means more volatility but pretty long ascend to the top.

Multi-year bull and an ATH surprising even to the biggest bulls as the infinite Cantillon "wealth" is pumped into crypto

Crypto becomes the ultimate Cantillon insider circle-jerk.

2/ This will be one the most iconic ideological reversals in history, comparable to Google who was firmly against advertising but turned into the most powerful ad company ever.

3/ This scenario reminds me of the 90s privatization period in the post-socialist countries.

The regime transition allowed the communist party elite to benefit from the wild west form of "capitalism" that ensued, transferring (and multiplying) their wealth into the new regime.

4/ We are far from Satoshi's original vision . But words and intentions of *prophets* were used to manipulate and corrupt all throughout human history and this time it is no

Key difference between the '17 and roaring 20s in crypto is that back then everyone was aping a16z and Naval.

Today everyone apes 3AC wanting to be the next Degen.

'17 was an idealistic *saving the world* kind of thing

20s is *me against the world*

1/ The financialization of crypto means more volatility but pretty long ascend to the top.

Multi-year bull and an ATH surprising even to the biggest bulls as the infinite Cantillon "wealth" is pumped into crypto

Crypto becomes the ultimate Cantillon insider circle-jerk.

2/ This will be one the most iconic ideological reversals in history, comparable to Google who was firmly against advertising but turned into the most powerful ad company ever.

3/ This scenario reminds me of the 90s privatization period in the post-socialist countries.

The regime transition allowed the communist party elite to benefit from the wild west form of "capitalism" that ensued, transferring (and multiplying) their wealth into the new regime.

4/ We are far from Satoshi's original vision . But words and intentions of *prophets* were used to manipulate and corrupt all throughout human history and this time it is no

At "forever" Cantillon insiders are infinitely wealthy. Everybody else lives in pods & eats what the livestock eats, or joins the harem or household staff of an infinitaire.

— Nick Szabo (@NickSzabo4) January 21, 2020

1/ A thread on Nexgen’s Arrow & the #uranium cycle ($NXE)

2/ Given the scale and cost structure of Arrow, it makes sense that investors are intensely focused on its delivery timeline. This thread will discuss possible timelines, current market expectations (i.e., what’s “priced in”) & how different Arrow scenarios will impact the mkt.

3/ As you can see from the litany of responses to Michael’s tweet, there is great skepticism in the market regarding Arrow’s timeline. This is largely due to a bearish narrative conveyed by competing CEO’s whose assets only hold value if Arrow is substantially delayed.

4/ Those who played “King of the Hill” as a child would remember that it is the person at the top who is constantly attacked, not the kid sitting at the bottom of the hill in the mud. No one cares enough about that kid to attack them. This is a good parable for $NXE & Uranium.

5/ First a quick note on “this cycle” – Segra generally defines this cycle as the deficits forecasted from the mid-2020s to late-2030s. When people imply an asset producing in the mid-to-late 2020s will “miss the cycle”, they clearly have not done any real S/D modelling.

Can anyone tell me an estimated time frame that Nexgen could be permitted, start building their mine and be producing #uranium ??? @quakes99 @JekyllCapital @travmcph @NexGenEnergy $nxe

— Michael Pierce (@Big_U_Dawg) January 22, 2021

2/ Given the scale and cost structure of Arrow, it makes sense that investors are intensely focused on its delivery timeline. This thread will discuss possible timelines, current market expectations (i.e., what’s “priced in”) & how different Arrow scenarios will impact the mkt.

3/ As you can see from the litany of responses to Michael’s tweet, there is great skepticism in the market regarding Arrow’s timeline. This is largely due to a bearish narrative conveyed by competing CEO’s whose assets only hold value if Arrow is substantially delayed.

4/ Those who played “King of the Hill” as a child would remember that it is the person at the top who is constantly attacked, not the kid sitting at the bottom of the hill in the mud. No one cares enough about that kid to attack them. This is a good parable for $NXE & Uranium.

5/ First a quick note on “this cycle” – Segra generally defines this cycle as the deficits forecasted from the mid-2020s to late-2030s. When people imply an asset producing in the mid-to-late 2020s will “miss the cycle”, they clearly have not done any real S/D modelling.

You May Also Like

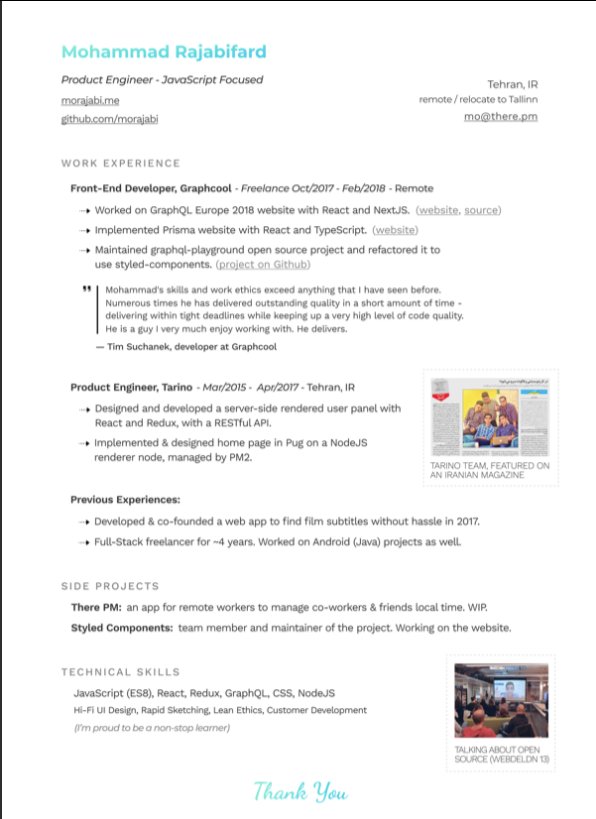

👨💻 Last resume I sent to a startup one year ago, sharing with you to get ideas:

- Forget what you don't have, make your strength bold

- Pick one work experience and explain what you did in detail w/ bullet points

- Write it towards the role you apply

- Give social proof

/thread

"But I got no work experience..."

Make a open source lib, make a small side project for yourself, do freelance work, ask friends to work with them, no friends? Find friends on Github, and Twitter.

Bonus points:

- Show you care about the company: I used the company's brand font and gradient for in the resume for my name and "Thank You" note.

- Don't list 15 things and libraries you worked with, pick the most related ones to the role you're applying.

-🙅♂️"copy cover letter"

"I got no firends, no work"

One practical way is to reach out to conferences and offer to make their website for free. But make sure to do it good. You'll get:

- a project for portfolio

- new friends

- work experience

- learnt new stuff

- new thing for Twitter bio

If you don't even have the skills yet, why not try your chance for @LambdaSchool? No? @freeCodeCamp. Still not? Pick something from here and learn https://t.co/7NPS1zbLTi

You'll feel very overwhelmed, no escape, just acknowledge it and keep pushing.

- Forget what you don't have, make your strength bold

- Pick one work experience and explain what you did in detail w/ bullet points

- Write it towards the role you apply

- Give social proof

/thread

"But I got no work experience..."

Make a open source lib, make a small side project for yourself, do freelance work, ask friends to work with them, no friends? Find friends on Github, and Twitter.

Bonus points:

- Show you care about the company: I used the company's brand font and gradient for in the resume for my name and "Thank You" note.

- Don't list 15 things and libraries you worked with, pick the most related ones to the role you're applying.

-🙅♂️"copy cover letter"

"I got no firends, no work"

One practical way is to reach out to conferences and offer to make their website for free. But make sure to do it good. You'll get:

- a project for portfolio

- new friends

- work experience

- learnt new stuff

- new thing for Twitter bio

If you don't even have the skills yet, why not try your chance for @LambdaSchool? No? @freeCodeCamp. Still not? Pick something from here and learn https://t.co/7NPS1zbLTi

You'll feel very overwhelmed, no escape, just acknowledge it and keep pushing.