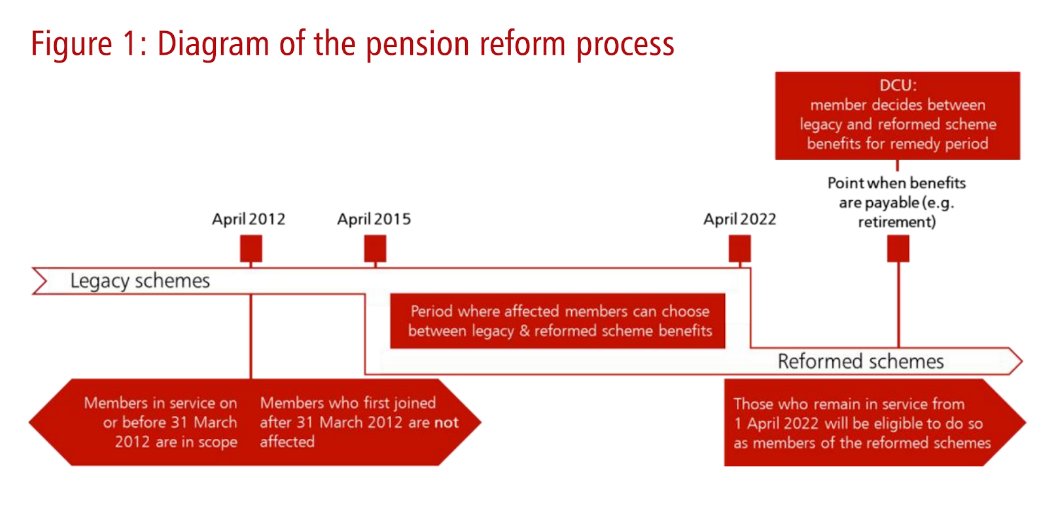

Broadly in 1995 (or “legacy”) pension scheme, each year you got 1/80th of your “final salary” as a pension & 3/80th a tax free lump sum

1/ A thread [1/2]about your NHS pensions, tax & the age discrmination “McCloud” case👇

OK this is complicated stuff, Im going to take you through it step by step. But its important, and will affect your pension, so buckle up and pay attention!

Please share & RT/share awareness

Broadly in 1995 (or “legacy”) pension scheme, each year you got 1/80th of your “final salary” as a pension & 3/80th a tax free lump sum

● CARE (not fin sal)

● 1/54ths (not 80ths/60ths), “revalued” at 1.5%/yr

● State pension age (not 60 or 65)

● Final salary link maintained for pre-2015 pension

Government ignored him and decided to either fully protect those closest (full protection) or just behind this cohort (tapered protection)

Whoops

contin/ 26.. https://t.co/jSvpkEyzj0

Cont\U0001f447

— Dr Tony Goldstone \U0001f499 (@goldstone_tony) February 13, 2021

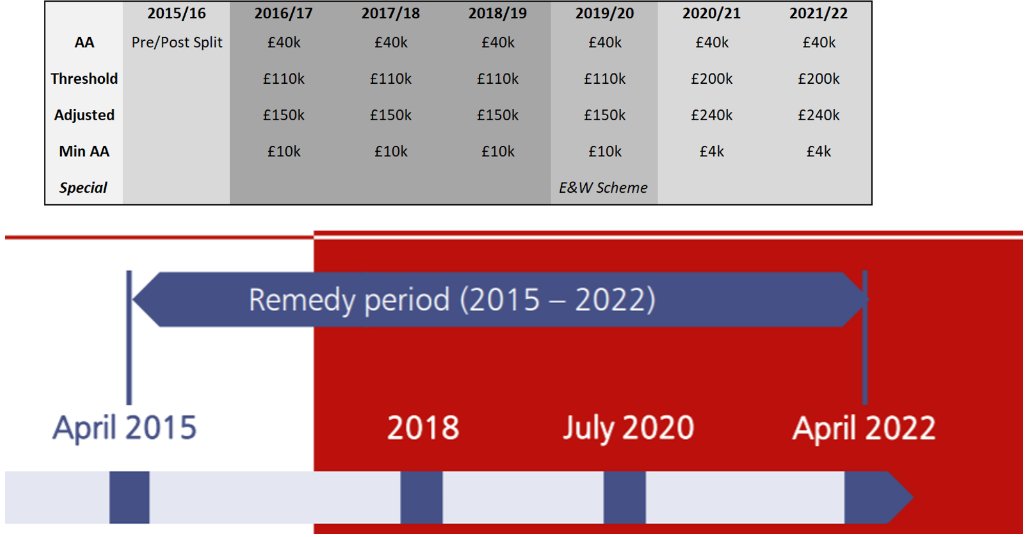

26/ If you have paid AA tax between 1995-22 it is likely your charges will be lower in 1995 than in 2015 scheme. This is because the AA rules are particularly unfair to members of 2 schemes. If your AA charges go down during any of the remedy period, you can claim a refund

More from Finance

Ivor Cummins has been wrong (or lying) almost entirely throughout this pandemic and got paid handsomly for it.

He has been wrong (or lying) so often that it will be nearly impossible for me to track every grift, lie, deceit, manipulation he has pulled. I will use...

... other sources who have been trying to shine on light on this grifter (as I have tried to do, time and again:

Example #1: "Still not seeing Sweden signal versus Denmark really"... There it was (Images attached).

19 to 80 is an over 300% difference.

Tweet: https://t.co/36FnYnsRT9

Example #2 - "Yes, I'm comparing the Noridcs / No, you cannot compare the Nordics."

I wonder why...

Tweets: https://t.co/XLfoX4rpck / https://t.co/vjE1ctLU5x

Example #3 - "I'm only looking at what makes the data fit in my favour" a.k.a moving the goalposts.

Tweets: https://t.co/vcDpTu3qyj / https://t.co/CA3N6hC2Lq

He has been wrong (or lying) so often that it will be nearly impossible for me to track every grift, lie, deceit, manipulation he has pulled. I will use...

... other sources who have been trying to shine on light on this grifter (as I have tried to do, time and again:

Ivor Cummins BE (Chem) is a former R&D Manager at HP (sourcre: https://t.co/Wbf5scf7gn), turned Content Creator/Podcast Host/YouTube personality. (Call it what you will.)

— Steve (@braidedmanga) November 17, 2020

Example #1: "Still not seeing Sweden signal versus Denmark really"... There it was (Images attached).

19 to 80 is an over 300% difference.

Tweet: https://t.co/36FnYnsRT9

Example #2 - "Yes, I'm comparing the Noridcs / No, you cannot compare the Nordics."

I wonder why...

Tweets: https://t.co/XLfoX4rpck / https://t.co/vjE1ctLU5x

Example #3 - "I'm only looking at what makes the data fit in my favour" a.k.a moving the goalposts.

Tweets: https://t.co/vcDpTu3qyj / https://t.co/CA3N6hC2Lq

You May Also Like

Krugman is, of course, right about this. BUT, note that universities can do a lot to revitalize declining and rural regions.

See this thing that @lymanstoneky wrote:

And see this thing that I wrote:

And see this book that @JamesFallows wrote:

And see this other thing that I wrote:

One thing I've been noticing about responses to today's column is that many people still don't get how strong the forces behind regional divergence are, and how hard to reverse 1/ https://t.co/Ft2aH1NcQt

— Paul Krugman (@paulkrugman) November 20, 2018

See this thing that @lymanstoneky wrote:

And see this thing that I wrote:

And see this book that @JamesFallows wrote:

And see this other thing that I wrote: