They find the property, do all the work, hire the management company and take fees. They often co-sign debt and always secure the financing.

A THREAD on how most real estate folks structure deals with outside investors.

Most people utilize the "preferred equity" structure when they raise money from outside investors. They "syndicate" deals.

Here's the basics:

They find the property, do all the work, hire the management company and take fees. They often co-sign debt and always secure the financing.

They don't co-sign debt. They simply read reports and ask the sponsors questions and cash checks every month (if the deal is going well).

"Preferred equity" belongs to the LPs. Cash talks, so this is a higher class of shares. They are first in the "capital stack" behind the debt (bank loan).

"Common equity" belongs to the sponsor. They are generally last in the capital stack.

That means the GP has skin in the game. His 10% co-invest makes him both an LP and a GP.

That means they get paid first. The pref signals how much. Its generally 6-12%. That means the LP is entitled to the first 6-12% of profit the project generates.

New development, or high risk value add projects, generally warrant lower prefs and higher "promotes"

Its a percentage of profits the sponsor gets AFTER the LPs get their preferred return on their cash.

This ranges from 20% to 50%. It can change based on checkpoints, or "waterfall".

Because every day your LP capital isn't returned its accumulating "preferred returns" that you owe to the LP. The only way to stop it is to return it.

There are often additional waterfalls. 80/20 after an 8 pref and 50/50 after a 20% "hurdle".

A hurdle is a return percentage you need to hit to get into the next level of promote.

Internal Rate of Return.

When the deal is done, and my capital is back, what percent return have I earned?

Sponsors hate it because there are so many other factors that are more important to the health of the deal.

How long of a time frame are we on? These deals aren't liquid. LPs can't just ask for their money back.

Sponsors lay out the investment timeline and let everyone know how long this thing is expected to go.

Acquisition fees can be anywhere from 1-5%.

AUM fees are generally .5-2%.

The market sets these fees (as well as the pref and promote). If you have a track record, more fees.

I buy storage facilities so lets say we have a $1MM operational facility already at 90% occupancy.

Its (relatively) low risk so lets say the structure is 7 pref and 50% promote thereafter. No waterfalls.

We raise 300k from outside LPs to close out the deal. No co-invest to keep the math simple.

Starting on day 1 we owe the LPs a 7% annual rate (pref) on the $300k.

I would get paid $50k on day one to buy the deal and get it under ownership.

To keep the math simple we aren't building this in, but keep it in mind.

The 1% AUM fee would be $3,000 a year on the $300k.

That goes to the sponsor.

Our cash on cash would be around 15% or higher if we can secure Interest Only debt (not paying principle for the first period of time).

That means on day one I'm hitting the hurdle and getting paid

But we have $45k in cashflow, or $24k after the pref.

That money is split 50/50 between the GP and the LPs because we have a 50% promote.

Yr 1 the LPs get $21k+$12k for $33k. 11% IRR pace.

Yr 2 cashflow is even higher, $45k+$30k for $75k.

LPs are owed $21k as their pref and we have more to split up between the sponsor and LPs. LPs get another $27k and Sponsors get $27k.

Lets do a sale first. Our property might be worth a 7 cap on the new NOI, or $1.428MM. Lets say $1.5 for simple math.

We sell it for $1.5M at the 24 month mark. Home run deal.

Bank gets their $700k back first.

LPs get their $300k back next.

They've already been getting their pref from day 1 so we don't have a preferred return to "catch up" when we sell. So its 50/50 from here.

In 24 months the LPs made $81k in cashflow (or 13.5% per year).

That means the targeted cash yield on the deal should have been around 13.5% if the sponsors projections were correct. Cash yield doesn't account for sale, only ops.

A $331k total profit. In 2 yrs.

IRR: 55.16%

Equity Multiple: 2.1x

Add it to your resume, pay a bunch of taxes, and do a bigger deal!

Instead of selling the property for $1.5MM and paying a bunch of taxes and being stuck with $500k in capital that is earning nothing and needs re-deployed, lets hold the asset and put more debt on it.

They get the property appraised for $1.5MM, look at the debt service coverage ratio, and agree to lend 75% of the new value.

That means you can take $1,125,000 in new debt.

Bank gets paid $700k (original debt is cleared).

LPs get paid $300k (original investment, pref is no longer accruing)

You have $125k left over. Sponsor gets 50%. LPs get 50%.

EVERYTHING FROM HERE IS BUTTER.

The property still cashflows. You didn't pay a bunch of taxes. You still got LPs their money back and they're ready to do another deal with you.

You as the sponsor, now own 50% of a building you put $0 into.

I'm not a pro at this. Looking forward to getting corrected where I missed something.

There are thousands of ways to do this and terms and factors I didn't mention.

I just wish I could have read something like this a year ago when I first started on ReTwit.

https://t.co/h4fybmycuK

I use @GroundbreakerCo to manage my LPs. Same thing as Juniper Square except 1/5 the cost. Love it.

https://t.co/FEt1sBoSWS

More from Nick Huber

Don’t have much cash but want to invest in real estate?

Want to get SBA loans and special loan programs so you can buy real estate investments with only 5-10% down?

One word for you:

Don’t.

Here’s why

👇👇👇

Leverage can be a beautiful thing.

Appreciation takes over and all that value you bought with debt grows and you amplify your returns.

But there is another, darker side of debt.

Values drop 5 or 10% and you’re underwater. You have zero equity or negative equity.

Ask the folks who were over-levered in 2007 what happened on 2011?

Real estate is a frothy space right now. Money flying everywhere and values higher than they’ve ever been.

Debt is cheaper and easier to get than ever.

Will it continue?

Probably.

Money could stay cheap for a long time. There is a ton of negative yielding debt abroad and liquidity ready to flood our market at the drop of a hat.

Rates will likely stay low. Gov will probably keep subsidizing these loans. You’ll probably be okay.

Want to get SBA loans and special loan programs so you can buy real estate investments with only 5-10% down?

One word for you:

Don’t.

Here’s why

👇👇👇

Leverage can be a beautiful thing.

Appreciation takes over and all that value you bought with debt grows and you amplify your returns.

But there is another, darker side of debt.

Everybody I know loves LEVERAGE when it comes to real estate.

— Nick Huber (@sweatystartup) October 18, 2020

It\u2019s a beautiful and scary tool, kicking appreciation, depreciation, and cashflow into overdrive.

It amplifies everything. You can make a lot of money really fast and go broke in months.

Here\u2019s how it works\U0001f447\U0001f447\U0001f447

Values drop 5 or 10% and you’re underwater. You have zero equity or negative equity.

Ask the folks who were over-levered in 2007 what happened on 2011?

Real estate is a frothy space right now. Money flying everywhere and values higher than they’ve ever been.

Debt is cheaper and easier to get than ever.

Will it continue?

Probably.

Money could stay cheap for a long time. There is a ton of negative yielding debt abroad and liquidity ready to flood our market at the drop of a hat.

Rates will likely stay low. Gov will probably keep subsidizing these loans. You’ll probably be okay.

More from Business

The Mother of All Squeezes

How Volkswagen went from being on the brink of bankruptcy to the most valuable company in the world in two days

/THREAD/

1/ At the peak of the 2008 financial crisis, Volkswagen was considered a very likely candidate for bankruptcy.

Heavily indebted and already financially struggling before 2008, with car sales expected to plummet due to the ongoing global crisis.

2/ With GM and Chrysler filing for bankruptcy in 2009, shorting the VW stock would seem a safe bet.

If you are not familiar with stock shorts and short squeezes check my thread

3/ On October 26, 2008, Porsche announced it had increased its stake at VW from 30% to 74%.

This was a surprise to many who were led to believe that Porsche wasn't planning a takeover of VW, based on the company's announcements.

4/ Before the announcement, the short interest was approximately 13% of the outstanding shares, a number considered relatively low.

Porsche had a 30% stake, the Lower Saxony government fund held 20% of the shares, and another 5% was held by index funds.

How Volkswagen went from being on the brink of bankruptcy to the most valuable company in the world in two days

/THREAD/

1/ At the peak of the 2008 financial crisis, Volkswagen was considered a very likely candidate for bankruptcy.

Heavily indebted and already financially struggling before 2008, with car sales expected to plummet due to the ongoing global crisis.

2/ With GM and Chrysler filing for bankruptcy in 2009, shorting the VW stock would seem a safe bet.

If you are not familiar with stock shorts and short squeezes check my thread

Shorts, Squeezes, and Betting Against Stocks

— Kostas on FIRE \U0001f525 (@itsKostasOnFIRE) January 27, 2021

What is short selling, how is it used and why is it risky?

/THREAD/ pic.twitter.com/PyDd208hFe

3/ On October 26, 2008, Porsche announced it had increased its stake at VW from 30% to 74%.

This was a surprise to many who were led to believe that Porsche wasn't planning a takeover of VW, based on the company's announcements.

4/ Before the announcement, the short interest was approximately 13% of the outstanding shares, a number considered relatively low.

Porsche had a 30% stake, the Lower Saxony government fund held 20% of the shares, and another 5% was held by index funds.

Should we go into the details of these 125 years?

SA is built on the exploitation of labour. That labour has functioned on alcohol unfortunately. Very few people consume liquor purely for enjoyment unfortunately. When SAB opened its doors 1895 workers were paid in alcohol- the dop/tot system. 2 years into SAB's establishment

The Prohibition Act is introduced. This means black people are barred from buying your wines, beer etc. So SAB's products are exclusively for white people. But during this period beer brewing by Black women is the norm. Ayinxilisi ncam ke this type of beer. Apparently it had some

Nutritious elements to it. Now some of the context around drinking culture during this time is migrant labour to the mines, further land dispossession, the Anglo-Boer Wars, Rhodes corruption (our first state capture commission if you will) which leads to his resignation.

This context plays a role in how our cities and small towns are constructed, how they lead to the confinement and surveillance yabantu. Traditional beer brewing is identified as a threat because buy now mining bosses have identified that there's money to be made here.

SAB has formed part of the fabric of SA for the last 125 years & we've stood behind the nation through its triumphs & challenges. After much consideration,SAB has decided to approach the Courts to challenge the Constitutionality of the decision taken to re-ban the sale of alcohol pic.twitter.com/40rWpJSW5b

— SABreweries (@SABreweries) January 6, 2021

SA is built on the exploitation of labour. That labour has functioned on alcohol unfortunately. Very few people consume liquor purely for enjoyment unfortunately. When SAB opened its doors 1895 workers were paid in alcohol- the dop/tot system. 2 years into SAB's establishment

The Prohibition Act is introduced. This means black people are barred from buying your wines, beer etc. So SAB's products are exclusively for white people. But during this period beer brewing by Black women is the norm. Ayinxilisi ncam ke this type of beer. Apparently it had some

Nutritious elements to it. Now some of the context around drinking culture during this time is migrant labour to the mines, further land dispossession, the Anglo-Boer Wars, Rhodes corruption (our first state capture commission if you will) which leads to his resignation.

This context plays a role in how our cities and small towns are constructed, how they lead to the confinement and surveillance yabantu. Traditional beer brewing is identified as a threat because buy now mining bosses have identified that there's money to be made here.

You May Also Like

A THREAD ON @SarangSood

Decoded his way of analysis/logics for everyone to easily understand.

Have covered:

1. Analysis of volatility, how to foresee/signs.

2. Workbook

3. When to sell options

4. Diff category of days

5. How movement of option prices tell us what will happen

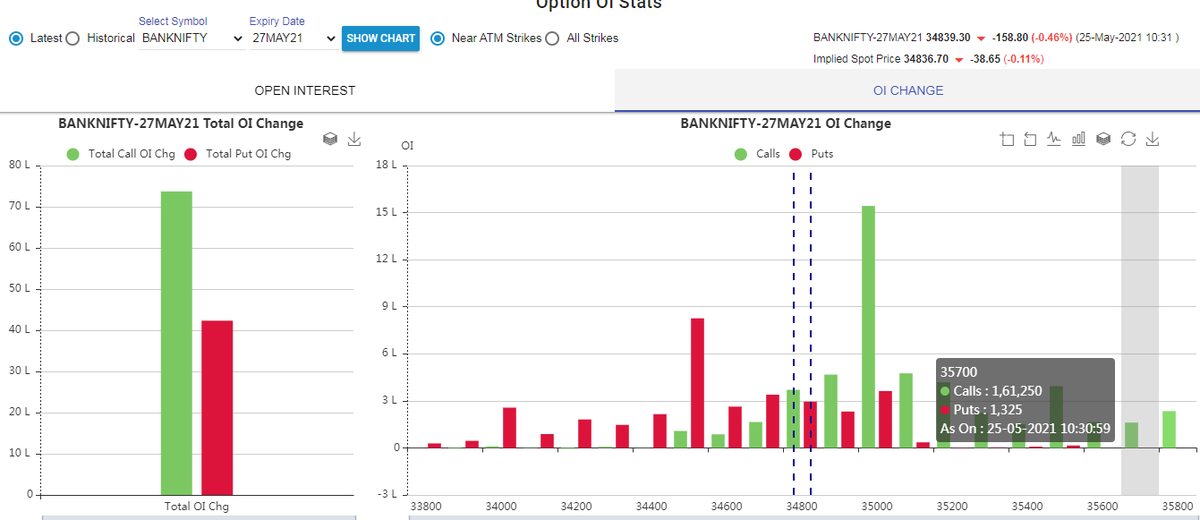

1. Keeps following volatility super closely.

Makes 7-8 different strategies to give him a sense of what's going on.

Whichever gives highest profit he trades in.

2. Theta falls when market moves.

Falls where market is headed towards not on our original position.

3. If you're an options seller then sell only when volatility is dropping, there is a high probability of you making the right trade and getting profit as a result

He believes in a market operator, if market mover sells volatility Sarang Sir joins him.

4. Theta decay vs Fall in vega

Sell when Vega is falling rather than for theta decay. You won't be trapped and higher probability of making profit.

Decoded his way of analysis/logics for everyone to easily understand.

Have covered:

1. Analysis of volatility, how to foresee/signs.

2. Workbook

3. When to sell options

4. Diff category of days

5. How movement of option prices tell us what will happen

1. Keeps following volatility super closely.

Makes 7-8 different strategies to give him a sense of what's going on.

Whichever gives highest profit he trades in.

I am quite different from your style. I follow the market's volatility very closely. I have mock positions in 7-8 different strategies which allows me to stay connected. Whichever gives best profit is usually the one i trade in.

— Sarang Sood (@SarangSood) August 13, 2019

2. Theta falls when market moves.

Falls where market is headed towards not on our original position.

Anilji most of the time these days Theta only falls when market moves. So the Theta actually falls where market has moved to, not where our position was in the first place. By shifting we can come close to capturing the Theta fall but not always.

— Sarang Sood (@SarangSood) June 24, 2019

3. If you're an options seller then sell only when volatility is dropping, there is a high probability of you making the right trade and getting profit as a result

He believes in a market operator, if market mover sells volatility Sarang Sir joins him.

This week has been great so far. The main aim is to be in the right side of the volatility, rest the market will reward.

— Sarang Sood (@SarangSood) July 3, 2019

4. Theta decay vs Fall in vega

Sell when Vega is falling rather than for theta decay. You won't be trapped and higher probability of making profit.

There is a difference between theta decay & fall in vega. Decay is certain but there is no guaranteed profit as delta moves can increase cost. Fall in vega on the other hand is backed by a powerful force that sells options and gives handsome returns. Our job is to identify them.

— Sarang Sood (@SarangSood) February 12, 2020